Table of Contents >> Show >> Hide

- What People Mean by “Lost Decade” (and Why Definitions Matter)

- The Last “Lost Decade” (2000–2009): What Actually Happened

- How Lost Decades Happen (Without the World Ending)

- Are the Ingredients for Another Lost Decade Present Today?

- What Investors Can Control If Returns Get Boring

- A Quick Stress Test: “What If Returns Are Half of What I’m Used To?”

- So… Could We See Another Lost Decade?

- Experiences: What Living Through a Lost Decade Teaches You (About )

- SEO Tags

“Lost decade” sounds like your portfolio wandered into the woods, forgot its GPS, and started living off berries.

In investing, it usually means something simpler (and more annoying): a long stretch where broad U.S. stock returns

are flat-ish, choppy, or disappointingespecially after inflation.

The uncomfortable truth: a lost decade doesn’t require economic doom, a meteor, or your neighbor becoming a “full-time crypto philosopher.”

It can happen when stock prices start expensive, profits grow at a normal pace, and valuations quietly deflate like a sad birthday balloon.

The good news: even when markets go sideways, investors still have levers they can pullwithout trying to outsmart every headline.

What People Mean by “Lost Decade” (and Why Definitions Matter)

Price return vs. total return

When people say “the market did nothing for 10 years,” they’re often looking at pricethe index level.

But investors earn total return: price changes plus dividends (and sometimes buybacks indirectly through earnings per share).

Dividends can turn “meh” decades into “still not fun, but survivable” decadesespecially if reinvested.

Nominal return vs. real return

Then there’s inflationthe invisible gremlin that eats purchasing power.

A decade of low nominal returns can feel much worse if inflation is high.

That’s why some “lost decades” are really lost purchasing-power decades.

Bottom line: the phrase “lost decade” is a vibe, not a scientific unit.

It usually means “my money didn’t grow the way I assumed it would,” and that’s exactly the risk worth planning for.

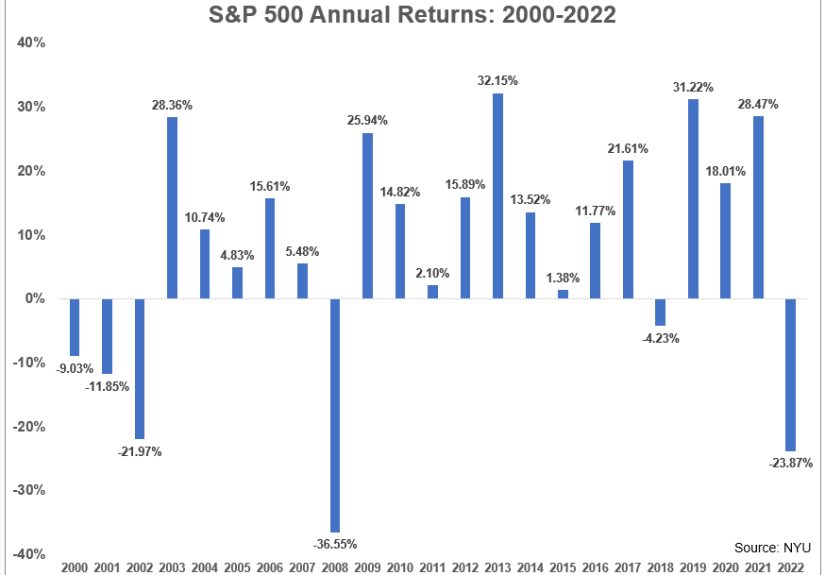

The Last “Lost Decade” (2000–2009): What Actually Happened

The most famous modern U.S. example is the 2000s, when U.S. large-cap stocks delivered unusually weak results for many investors.

It wasn’t one disasterit was a two-hit combo.

Two crashes, two recessions

The decade opened with the dot-com bust and closed with the global financial crisis.

The U.S. also experienced a recession in the early 2000s and the deep 2007–2009 recession.

When markets suffer big drawdowns early and then again later, even a recovery can feel like running on a treadmill set to “existential.”

The valuation hangover

The late 1990s left U.S. equities priced for perfection.

When expectations are sky-high, companies don’t have to do badly for investors to have a bad time.

If profits grow “normally” while valuations fall from “wow” back toward “okay,” returns can be muted for years.

Diversification was a lifeboat

One of the most underappreciated lessons from the 2000s is that the pain wasn’t uniform.

International stocks, value-leaning segments, and high-quality bonds often behaved very differently than U.S. large-cap growth.

Investors who held a diversified mix and rebalanced had more ways to “win by not losing.”

The 2000s were a reminder that the market can be a long-term wealth engine while still being a short-to-medium-term chaos machine.

How Lost Decades Happen (Without the World Ending)

Lost decades typically show up when a few forces line up.

None of them are exotic. All of them are stubborn.

1) High starting valuations

Stock returns come from some combination of earnings growth, dividends, and changes in valuation (how much investors are willing to pay per dollar of earnings).

When valuations start high, future returns are often lowernot because the market is “due” for punishment, but because math is rude.

If you pay more for the same stream of profits, your expected return drops.

2) Higher interest rates and the discount-rate effect

When safer bond yields rise, investors often demand a higher return from stocks too.

That can pressure stock valuations, especially for companies whose cash flows are expected far in the future (the classic “growth stock” story).

This is one reason markets can struggle even while the economy is still growing.

3) Inflation surprises

Inflation can hurt in two ways: it reduces real returns and can lead to tighter monetary policy (which can also compress valuations).

Even if corporate revenues rise with prices, higher input costs and higher discount rates can offset the benefit.

4) Profit margins and mean reversion

U.S. corporate profit margins have been historically strong in recent years.

If margins stay elevated, great.

If competition, regulation, labor costs, or slower demand pull margins down, earnings growth can disappointespecially from a high starting point.

5) Market concentration and narrow leadership

When a small group of mega-cap companies drives a large share of index returns, the market becomes more sensitive to that group’s fortunes.

If leadership narrows and then reversesbecause of valuation, regulation, competition, or simply changing narrativesbroad index returns can flatten out.

Are the Ingredients for Another Lost Decade Present Today?

The honest answer is: it’s possible, but the future is not a courtroom drama where we slam down one piece of evidence and yell “Objection!”

Markets are probabilistic.

So let’s look at the strongest arguments on both sides.

The case for “Yes, it could happen”

-

Valuations have been elevated at times: When broad market valuation measures run hot, long-run expected returns tend to cool.

That doesn’t mean a crash is guaranteedjust that the “easy mode” years may be behind us. -

Interest rates are no longer near-zero: Higher yields can compete with stocks and can pressure valuation multiples.

A world of “cash pays something” is a different investing climate than a world of “cash pays vibes.” -

Concentration risk: If a handful of giant companies make up a large chunk of index weight, disappointment in that group can drag the whole index.

Even if the broader economy does fine, the index can struggle if the most expensive leaders come back to earth. - Inflation uncertainty: If inflation remains sticky or volatile, it can make both corporate planning and investor expectations messieroften a recipe for lower valuation multiples.

The case for “Maybe not”

-

Innovation and productivity are real: New technology waves can lift productivity, profits, and business formation.

If innovation translates into broad earnings growth (not just hype), returns can stay healthier than valuation-based forecasts suggest. - U.S. companies are globally diversified: Many large U.S. firms earn significant revenue abroad, which can soften the impact of domestic slowdowns.

- Dividends and buybacks still matter: Even if prices move sideways, shareholders can still receive meaningful total return through cash distributions and compounding earnings.

-

Markets can stay expensive longer than you expect: Valuations are informative but not a stopwatch.

They often explain outcomes over a decade, not next quarter.

The most realistic middle ground

A “lost decade” doesn’t have to mean negative returns.

It can look like:

- lower-than-historical-average returns (especially after inflation),

- sharp rallies followed by sharp pullbacks (headline whiplash),

- periods where diversification beats picking the “best” U.S. index fund,

- and a big gap between what worked recently and what works next.

If you’re hoping for a simple forecast, here it is: the next decade is unlikely to hand out effortless double-digit annual returns with the consistency of a vending machine.

But it also doesn’t need to be catastrophic to feel “lost” compared to expectations.

What Investors Can Control If Returns Get Boring

If the market serves a decade of lukewarm returns, the winning move is rarely “do more stuff.”

It’s usually “do the right boring stuffmore consistently.”

Diversify beyond one index and one country

Many investors treat the S&P 500 like it’s synonymous with “stocks.”

It’s not.

A globally diversified stock allocation can reduce dependence on one market’s valuation cycle.

The 2000s were a vivid reminder that leadership rotatesand sometimes it rotates for longer than your patience.

Rebalance: the quiet superpower

Rebalancing forces you to trim what got expensive and add to what got cheaperbasically, it makes you do the opposite of panic.

In a choppy decade, this can be one of the few systematic ways to “buy low and sell high” without trying to predict the future.

Focus on savings rate and behavior

When returns are modest, the investor’s “input” matters more.

Contributions, time horizon, and staying invested can outweigh clever tactics.

The best portfolio is the one you can stick with when the news cycle is trying to emotionally mug you.

Watch sequence-of-returns risk near retirement

A lost decade hurts differently depending on when it shows up.

If you’re accumulating (still contributing), lower prices can be an opportunity.

If you’re withdrawing (retired or near retirement), early losses can be more damaging because you’re selling into weakness.

That’s why retirees often keep a buffer (like a bond/cash allocation) to avoid being forced sellers during downturns.

Keep costs, taxes, and “oops moments” low

In high-return decades, you can make small mistakes and still look like a genius.

In low-return decades, fees, taxes, and constant tinkering can quietly eat most of your gains.

If the next decade is lower-return, cost control becomes even more valuable.

Educational note: This article is for general information only, not individualized financial advice.

If you’re making major decisions, consider talking with a qualified financial professional.

A Quick Stress Test: “What If Returns Are Half of What I’m Used To?”

Here’s a useful mental exerciseno spreadsheets required.

-

Imagine your portfolio earns a healthy long-term return (say, something like historical averages).

Now imagine it earns roughly half that for 10 years. - Ask what would have to change: your savings rate, timeline, spending assumptions, or risk level.

- Identify which changes are within your controlthen pre-decide what you’d do if markets get choppy.

The point isn’t to be pessimistic.

It’s to prevent surprise from turning into bad decisions.

Investors rarely blow up because markets are volatile; they blow up because they didn’t plan for volatility to last.

So… Could We See Another Lost Decade?

Yes, it’s possibleespecially if high starting valuations, higher-for-longer interest rates, and concentrated leadership combine with slower earnings growth.

But “possible” isn’t the same as “inevitable,” and markets have a long history of embarrassing confident predictions.

A smarter framing is:

Can I build a plan that works even if U.S. stocks deliver a decade of mediocre real returns?

If the answer is yes, then whether the next decade is “lost” becomes less scaryand more like background noise.

Experiences: What Living Through a Lost Decade Teaches You (About )

People who lived through a flat decade in stocks often describe it as less like one dramatic crash and more like a long, stubborn emotional grind.

Not every day is terrible. Many days are fine. That’s the problembecause “fine” can lull you into expecting the next breakthrough rally to fix everything.

Then the market dips again, and you realize you’ve been stuck in a financial version of a slow-moving traffic jam.

The new investor experience: If you start investing near a market peak, the first few years can feel like being pranked by the universe.

You contribute regularly, read a few optimistic articles, and then watch your account wobble or go nowhere.

The lesson tends to be brutal but useful: your early returns are not your destiny, and consistency matters more than confidence.

Many long-term investors later say the habit of contributing through disappointment was the thing that made future bull markets work in their favor.

The mid-career autopilot experience: Investors who keep contributing through a choppy decade often come out okaynot because the market rewarded them quickly, but because they bought shares at many different prices.

Over time, those “boring” contributions can become the foundation of future gains.

The habit isn’t glamorous. It’s more like brushing your teeth: you don’t get applause, but you avoid pain.

The near-retiree experience: This is where a lost decade can feel personal.

If you’re close to using your portfolio, a big downturn early in retirement can sting because you may need withdrawals when prices are down.

People who experienced this often talk about the value of a cash/bond buffernot to “beat” the market, but to avoid being forced into the worst-timed sales.

The emotional relief of knowing you can pay bills without selling stocks at a discount is hard to overstate.

The rebalancer experience: Some investors discovered that rebalancing isn’t just a theory from textbooks.

In a sideways decade, rebalancing can feel like the only thing you do that’s both rational and measurable.

It forces you to trim what ran up and add to what got crushedexactly what your instincts may resist.

The people who stick to it often describe it as “uncomfortable in the moment, satisfying later.”

The biggest takeaway: A lost decade tests process more than intelligence.

It rewards the investor who can follow a reasonable plan while everyone else is reinventing theirs every six months.

If the next decade turns out to be slower, the winners probably won’t be the loudest voices on the internet.

They’ll be the ones quietly diversifying, controlling costs, rebalancing, and staying investeddoing the boring stuff that keeps working even when the market isn’t entertaining.