Table of Contents >> Show >> Hide

- What “Deep Risk” Really Means (And Why It’s Not Just Market Drama)

- Why Politics Can Become an Investing Variable

- The “Safe Harbor” Advantage: America’s Quiet Superpower

- Uncertainty Has a Price Tag (Even If It Doesn’t Show Up on Your Receipt)

- Trade Policy: A Case Study in “Rolling Uncertainty”

- Deep Risk Isn’t Only About MarketsIt’s About Trust

- What “Deep Risk Under President Trump” Means for Investors Today

- How to Invest When You Can’t Control the Headlines

- A Quick Reality Check: Markets Don’t Give Out “Best Behavior” Awards

- Conclusion: Deep Risk Is a Planning Problem, Not a Prediction Contest

- Experience Notes: of Real-World “Deep Risk” Moments (Composite Examples)

- 1) The small business owner who stopped signing long contracts

- 2) The retirement investor who “won” the market but lost sleep

- 3) The portfolio committee that added “governance risk” to the checklist

- 4) The “rule of law” conversation that suddenly felt less academic

- 5) The lesson people repeat after the anxiety passes

If you’ve ever watched the market react to a single headline like it just stepped on a Lego, you already understand shallow risk:

prices drop, people panic, and then (often) everything recovers after everyone finishes stress-eating cereal for dinner.

Deep risk is different. Deep risk is the “this changes the rules of the game” kind of riskthe type that can permanently reduce real wealth,

disrupt institutions, or rewrite expectations about what “normal” even means.

In early 2017, Ben Carlson at A Wealth of Common Sense framed the question many investors were quietly asking after Donald Trump’s election:

not “Will stocks go up or down next quarter?” but “What happens if the pillars that support market confidencerule of law, predictable regulation,

institutional stabilitystart to wobble?” That’s the heart of “deep risk under President Trump”: not day-to-day volatility, but the possibility of

lasting damage to the environment that makes investing work in the first place.

What “Deep Risk” Really Means (And Why It’s Not Just Market Drama)

The phrase “deep risk” is often associated with financial historian William Bernstein, who distinguishes between risks you can ride out and risks

you can’t. Shallow risk might leave you bruised and cranky for a while. Deep risk can leave you poorer in real terms for a long timeor permanently.

In plain English: shallow risk steals your sleep; deep risk steals your future purchasing power.

Deep risk doesn’t announce itself with a confetti cannon. It creeps in through structural cracks: unstable policy, weakened institutions, unpredictable

enforcement, loss of trust, or extreme macro shocks. And here’s the unfair part: deep risk can grow even when markets look “fine” on the surface.

The scoreboard (stock prices) can be up while the stadium (governance and trust) quietly catches fire.

Why Politics Can Become an Investing Variable

Most long-term investors want politics to be background noiselike the hum of an air conditioner you forget exists until it breaks. Markets are resilient.

Companies adapt. Consumers keep consuming. And history shows that markets have powered through wars, scandals, impeachments, and a truly impressive number

of terrible haircuts.

But political risk becomes investable risk when it threatens the underlying framework that allows capital to be priced and contracts to be trusted.

That framework includes:

- Rule of law: predictable enforcement of contracts and property rights.

- Institutional credibility: confidence that agencies, courts, and regulators function consistently.

- Policy stability: clarity on taxes, trade, spending, and regulatory direction.

- Information integrity: reliable economic data and transparent decision-making.

Carlson’s 2017 piece captured the anxiety that rapid, unpredictable governancepublic threats toward industries, corporations, or foreign partners,

frequent policy pivots, and a constant news cyclecould lead investors to demand a higher “risk premium” for U.S. assets. If investors require more

return to compensate for perceived instability, asset prices can fall even if earnings don’t.

The “Safe Harbor” Advantage: America’s Quiet Superpower

One reason U.S. markets have historically attracted global capital is the perception of stabilitywhat some economists describe as a “safe harbor”

premium. In that story, U.S. assets (especially Treasuries, but also U.S. equities) benefit from trust in American institutions, liquidity, and legal

protections. When the world feels shaky, money often runs toward the U.S., not away from it.

Research from The Budget Lab at Yale discusses how even modest changes in perceived U.S. political and institutional risk could have meaningful

long-run effectsby raising the cost of capital, reducing investment, and lowering household wealth over time. It’s a reminder that “country risk”

isn’t just something that happens in other places on a documentary you watch while folding laundry. It can be repriced anywhere if confidence erodes.

Uncertainty Has a Price Tag (Even If It Doesn’t Show Up on Your Receipt)

Uncertainty isn’t just a feeling. It’s measurableat least imperfectlythrough indexes built from news coverage and market reactions. The St. Louis Fed

publishes the U.S. Economic Policy Uncertainty (EPU) index, which tracks policy-related uncertainty using newspaper-based measures. When EPU spikes,

it often reflects moments when businesses and households feel less sure about what rules, costs, and conditions will look like.

Another related tool is the Fed’s “Equity Market Volatility Tracker” for trade policyan attempt to quantify how much trade policy news contributes to

market volatility. This matters because trade uncertainty can hit corporate planning fast: pricing, supply chains, contracts, and investment decisions

all get harder when tariff policies are announced, delayed, changed, or reversed.

How uncertainty becomes real economic behavior

Here’s the basic chain reaction: when uncertainty rises, firms delay irreversible decisions. Hiring slows. Capital spending gets postponed. Big projects

wait in a digital parking lot. That doesn’t always cause an immediate recessionbut it can shave growth, weaken confidence, and make the economy more

fragile to the next shock.

Trade Policy: A Case Study in “Rolling Uncertainty”

Trade policy is one of the clearest examples of how politics can transmit volatility into the real economy. If you run a business that imports components,

a tariff isn’t just a political statementit’s a cost line. If tariffs change frequently, you can’t price reliably, negotiate long-term supplier contracts

confidently, or forecast margins without building in a “chaos buffer.”

A Harvard Business School analysis of U.S. trade uncertainty notes that smaller firms can be hit especially hard because they lack the staff, legal resources,

and financial flexibility to constantly rework sourcing and pricing. Large multinationals can sometimes reroute supply chains; small businesses are more likely

to just absorb the blowor pass it on to customers and hope they don’t notice. (They notice.)

Deep Risk Isn’t Only About MarketsIt’s About Trust

Carlson revisited the “deep risk” theme in 2021 and made a striking point: markets had done relatively well through much of that period, but deeper concerns

had shifted toward the health of institutions and public trust. In other words, the biggest threat didn’t show up as a permanent market declineat least not

immediately. It showed up as a corrosion of confidence in governance and democratic stability.

That idea aligns with a broader view of systemic risk: the economy is not only factories and earnings; it’s also legitimacy, competence, and continuity. When

trust drops, everything gets more expensiveborrowing, investing, hiring, even basic public administration. And in extreme scenarios, institutional decay can

compound other risks (inflation, fiscal stress, geopolitical shocks) in nasty ways.

What “Deep Risk Under President Trump” Means for Investors Today

“Deep risk under President Trump” is not a claim that markets must crash under a particular administration. Markets are forward-looking, diversified,

and often stubbornly indifferent to commentary that makes humans spiral. The point is more practical: investors should consider how governance-related risks

could change the long-term investing environment.

For example, the Federal Reserve’s recent financial stability discussions highlight policy uncertainty and geopolitical risk among key concerns raised by

market participants. That doesn’t translate to “sell everything.” It translates to: uncertainty is part of the landscape, and it can interact with other

vulnerabilities (high leverage, higher rates, concentrated trades, fragile confidence).

Three ways deep risk can show up in a portfolio

-

Higher required returns (lower valuations): If investors demand more compensation for uncertainty, price-to-earnings multiples can compress

even if companies remain profitable. - Higher financing costs: If country risk rises, the cost of capital can rise, pressuring investment and long-run growth.

-

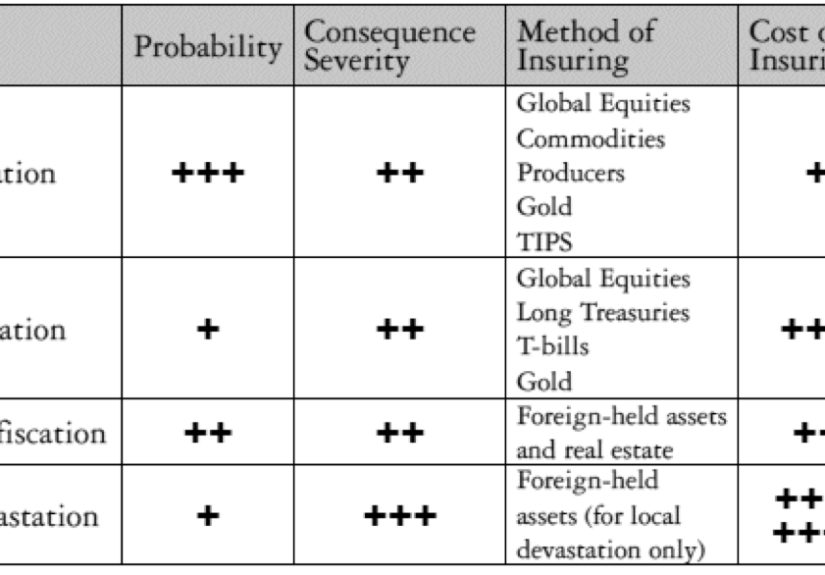

Inflation or policy shocks: Deep risk can be tied to rare but severe outcomespersistent inflation, confiscation-like policy changes, or

disruptions that permanently reduce real returns.

How to Invest When You Can’t Control the Headlines

The goal isn’t to predict politics (good luck with that). The goal is to build a portfolio that can survive a wide range of outcomes without requiring you to

become a full-time political forecaster with a side hustle as an amateur macro prophet.

1) Diversify like you mean it

Diversification isn’t a slogan; it’s a humility practice. A globally diversified portfolio can reduce the impact of country-specific shockseconomic,

political, or regulatory. That doesn’t mean abandoning U.S. assets. It means acknowledging that concentration risk is real, even when it’s wearing a

star-spangled outfit.

2) Own assets that respond differently to inflation

Deep risk often includes purchasing-power risk. A mix that includes inflation-sensitive components (as appropriate for your plan and risk tolerance) can help

if inflation becomes stubborn. The objective is not to “beat inflation this month,” but to protect long-run real wealth.

3) Keep liquidity for optionality

Liquidity is underrated because it’s boring. But during uncertain periods, liquidity buys you time, flexibility, and the ability to avoid selling long-term

assets at the worst possible moment. Think of it as financial WD-40.

4) Focus on what you can control

Your savings rate, fees, taxes, diversification, and behavior matter more than your ability to guess tomorrow’s headline. Deep risk is scary precisely because

it involves things outside your control. Your response should be a process that doesn’t depend on constant correct predictions.

A Quick Reality Check: Markets Don’t Give Out “Best Behavior” Awards

It’s tempting to believe markets reward good governance and punish bad governance instantlylike a cosmic teacher grading homework in real time. In reality,

markets can rally during messy periods and fall during calm ones. Price movements reflect expectations, liquidity, earnings, and global conditionsnot moral

judgments.

That’s why “deep risk” thinking is valuable: it asks you to pay attention to the foundation, not just the scoreboard. If the foundation weakens, the scoreboard

can still look fineuntil it doesn’t.

Conclusion: Deep Risk Is a Planning Problem, Not a Prediction Contest

“Deep Risk Under President Trump” remains useful because it frames political and institutional uncertainty as a portfolio design issue. The right response

isn’t panic. It’s preparation: diversify, respect inflation risk, maintain liquidity, and build a plan you can stick with even when the news cycle tries to

emotionally kidnap your brain.

If the next few years deliver only shallow riskordinary volatility and noisy headlinesgreat. Investors can live with that. But if deep risk emerges through

lasting institutional damage, persistent inflation, or policy instability that raises the cost of capital, you’ll be glad your plan was designed for more than

just “sunny-day investing.”

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice.

Experience Notes: of Real-World “Deep Risk” Moments (Composite Examples)

The tricky thing about deep risk is that most people don’t experience it as a single dramatic event. They experience it as a slow accumulation of “Wait… can they

do that?” moments. Below are composite, real-world-style experiences that mirror how investors and small businesses often feel uncertainty in practicewithout

pretending any single story represents everyone.

1) The small business owner who stopped signing long contracts

One importer of home goods (think: lighting fixtures, hardware, and those trendy cabinet pulls that cost more than a nice lunch) used to lock in supplier

contracts six to twelve months out. When tariff policy started changing frequentlyannounced, delayed, adjusted, re-announcedthe owner began shortening contract

timelines to 30–60 days. The business didn’t collapse, but it became more cautious: fewer bulk orders, smaller inventory buffers, more time spent renegotiating,

and higher prices passed to customers. That’s not a market crash. That’s uncertainty quietly taxing productivity.

2) The retirement investor who “won” the market but lost sleep

A near-retiree saw their portfolio hit new highs, but felt a persistent fear that the environment itself was less dependable: rising political conflict, more

aggressive rhetoric about institutions, and constant speculation about regulatory swings. Their behavior changed. They checked accounts more. They reduced equity

exposure too quickly. They held too much cash “just in case.” Ironically, the biggest damage wasn’t a bear marketit was decision fatigue and a portfolio that no

longer matched long-term goals. Shallow risk became personal because deep risk fear changed behavior.

3) The portfolio committee that added “governance risk” to the checklist

An investment committee at a midsize nonprofit began adding a new agenda item: “policy and governance watch.” Not because they wanted to trade headlines, but

because they wanted to stress-test assumptions: What if inflation runs hotter for longer? What if credit markets demand a higher premium? What if economic data

gets disrupted and forecasting becomes less reliable? They didn’t overhaul the portfolio monthly. They adjusted the plan oncemore global diversification, clearer

rebalancing rules, and a little extra liquidity. The emotional temperature went down because the process got stronger.

4) The “rule of law” conversation that suddenly felt less academic

Before 2017, some investors treated “rule of law” as a term that belonged in a textbook or a political science class. Then it became dinner-table conversation:

how agencies were staffed, whether institutions were respected, whether contracts and regulations would be applied consistently. Most days, nothing visibly broke.

But the shift in attention mattered. When a concept becomes a concern, it can affect willingness to pay premium valuations for assetsespecially if investors start

thinking, even subconsciously, “Maybe I should demand a bigger margin of safety.”

5) The lesson people repeat after the anxiety passes

The most common “experience takeaway” is boringbut true: the best defense against deep risk is not clairvoyance. It’s diversification, discipline, and a plan that

assumes the world can be weird for long stretches. People who had clear rules (automatic investing, rebalancing bands, cash reserves) generally handled uncertainty

better than those who tried to outguess every headline. The goal isn’t to be fearless; it’s to be structured enough that fear doesn’t become your portfolio manager.