Table of Contents >> Show >> Hide

- What Financial Independence Really Means Today

- The Three Levels Of Financial Independence

- Level 1: Budget (Lean) Financial Independence

- Level 2: Baseline (Comfortable) Financial Independence

- Level 3: Blockbuster (Abundant) Financial Independence

- How To Estimate Your Own FI Level

- Myths That Hold People Back From FI

- Designing Your Own Path Through The Three Levels

- Real-World Experiences With The Three Levels Of FI

If you’ve ever stared at your bank app and wondered, “Am I actually financially independent or just really good at pretending on Instagram?”you’re in the right place.

The idea of financial independence (FI) has exploded thanks to the FIRE movement (Financial Independence, Retire Early). At its core, FI means your investments and other passive income sources can cover your living expenses so work becomes optional, not mandatory. But as Sam Dogen of Financial Samurai famously points out, not all FI is created equal. There are different levels, different comfort zones, and very different emotional realities behind the same “I’m retired!” Instagram caption.

This article breaks down the three levels of financial independence inspired by Financial Samurai’s framework and blends it with what major financial sources say about FIRE, the 4% rule, and how much money people actually need to feel secure. We’ll also add real-world examples and experience-based insights so you can figure out where you are now, where you want to go, and what it really takes to get there.

What Financial Independence Really Means Today

Let’s define the basics before we climb the FI pyramid.

Most planners describe financial independence as the point where you have enough savings, investments, and cash flow to pay for your lifestyle indefinitely without relying on a full-time job. In FIRE circles, a common rule of thumb is the “Rule of 25”: you aim for a portfolio worth about 25 times your annual spending. That amount, paired with a roughly 4% initial withdrawal rate, is often used as a starting benchmark for a sustainable retirement income plan.

But here’s the catch: your lifestyle, location, health care costs, and family size can dramatically change what “enough” looks like. For someone living frugally in a low-cost area, financial independence at $30,000 per year of expenses feels realistic. For a family in a coastal city aiming for private schools, international travel, and high-end health coverage, “enough” might look more like $200,000+ per year.

That’s where the three levels come in. Instead of one magic number, you think in tierseach level offering more comfort, flexibility, and margin for error.

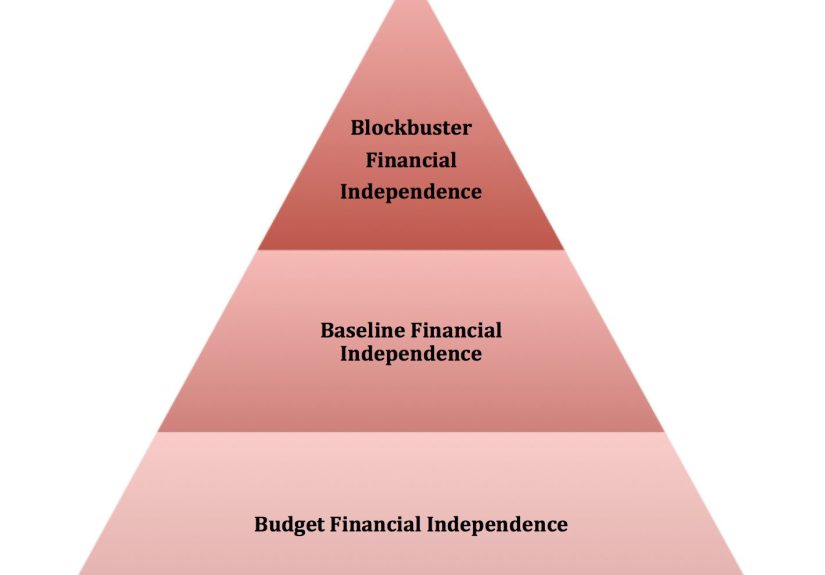

The Three Levels Of Financial Independence

Financial Samurai’s framework describes FI as a pyramid with three major tiers:

- Level 1: Budget (or Lean) Financial Independence – You’re “free,” but on a tight, minimalist budget.

- Level 2: Baseline (or Comfortable) Financial Independence – You can live a middle-to-upper-middle-class lifestyle without needing a job.

- Level 3: Blockbuster (or Abundant) Financial Independence – Work is strictly optional and your passive income supports a high-end lifestyle plus big goals.

Think of it like travel classes on a plane: Economy, Premium Economy/Business Lite, and First Class. All three get you to your destinationfreedom from mandatory workbut your experience along the way is very different.

Level 1: Budget (Lean) Financial Independence

Budget FI (often called Lean FIRE) is where your passive income covers a modest lifestyle with little room for luxury. You’re not pooryou’re just very deliberate. Every dollar has a job and none of those jobs involve bottle service.

What Budget FI Looks Like

Budget FI usually means:

- You live in a low or moderate cost-of-living area.

- Your housing costs are lowmaybe you share housing, live small, or your mortgage is tiny.

- You rarely finance big purchases and avoid lifestyle inflation.

- Vacations are budget-friendly: think road trips, off-season travel, or points hacking.

- Health insurance choices and medical costs require careful planning.

A typical Budget FI household might spend something like $30,000 to $50,000 a year. Using the Rule of 25, that translates to a portfolio in the ballpark of $750,000 to $1.25 million invested, assuming you’re comfortable with the risk, the withdrawal rate, and the fact that life rarely behaves like a spreadsheet.

Pros And Cons Of Budget FI

Upsides:

- It’s achievable faster, especially if you combine a strong income with frugality.

- You can leave a stressful job earlier and reclaim your time.

- You maintain the option to earn part-time income if needed, which many people do anyway.

Downsides:

- Unexpected expenses (medical, family, housing) can hit much harder.

- You may feel constant pressure to keep spending low.

- It can be emotionally tiring to say “no” to things you technically could afford but probably shouldn’t.

Many people who reach Budget FI eventually go back to some kind of worknot because they failed, but because they want more margin, more flexibility, or simply miss having bigger options.

Level 2: Baseline (Comfortable) Financial Independence

Baseline FI is where most people’s dreams live. Here, your investments and passive income support a lifestyle that feels solidly comfortable. You’re not rolling in superyacht money, but you can enjoy travel, hobbies, and nicer conveniences without constantly watching the grocery total.

Signs You’re At Baseline FI

People in this tier usually:

- Have housing secured in a decent neighborhood, often with a paid-off or nearly paid-off home.

- Can afford reliable transportation and basic travel each year.

- Save or set aside money for maintenance, health care, and emergencies.

- Can help with kids’ expenses, like extracurriculars or some college costs, if they choose.

- Don’t need to work, but might choose to for meaning, social life, or fun money.

Annual spending in Baseline FI might range from roughly $60,000 to $120,000 for a household, depending on location and goals. That implies a portfolio somewhere around $1.5 million to $3 million using the same 25x rule, though individual situations vary.

How People Move From Budget To Baseline FI

The move from Budget FI to Baseline FI is less about discovering a magical stock and more about good, boring habits:

- Continuing to invest even after reaching Budget FI instead of slamming the brakes.

- Shifting from purely frugal living to strategic spending that boosts long-term happiness (health, relationships, skills).

- Using part-time work, consulting, or a small business to bridge the gap and reduce stress on the portfolio.

- Diversifying income sources beyond just index fundssuch as real estate, small businesses, royalties, or online ventures.

This level often feels like the sweet spot: you’re not under pressure to consume or impress, but you can say “yes” to enough of the good stuff that life doesn’t feel like one long coupon-clipping marathon.

Level 3: Blockbuster (Abundant) Financial Independence

Blockbuster FI is the top of the pyramid. It’s the level that turns heads: high passive income, big safety margins, and the ability to support a more luxurious lifestyle or ambitious long-term projects.

Here, you might comfortably spend $200,000+ per year and still have plenty of buffer. Your portfolio is large enough that withdrawals are a smaller percentage of your total wealth, and you may also have significant equity in businesses, real estate, or other cash-flowing assets.

What Blockbuster FI Actually Feels Like

On paper, Blockbuster FI looks like endless vacation. In reality, it often looks like:

- Owning a primary home (often paid off) and possibly one or more rentals or vacation places.

- Investing heavily in businesses, private equity, or alternative assets.

- Being able to fund big goals: philanthropy, angel investing, multi-generational planning.

- Still workingbut on projects you truly care about rather than out of necessity.

People at this level often struggle less with “Can I afford this?” and more with questions like “What gives my life purpose now?” or “How do I use this money wisely?” The money problems don’t vanishthey simply move into a different category.

How To Estimate Your Own FI Level

You don’t have to guess where you are. You can do this with a simple exercise.

Step 1: Add Up Your Real Annual Spending

Look at your actual spending over the past 12 months, not your ideal budget. Include:

- Housing (rent or mortgage, taxes, insurance, utilities)

- Food and household expenses

- Transportation

- Health insurance and medical costs

- Childcare or education

- Debt payments

- Travel, fun, and little luxuries you actually buy

That total is your current lifestyle cost. Now ask: “If I tightened my belt without being miserable, how much could this drop?” That lower number is your Budget FI spending. Your current level might be closer to Baseline FI spending.

Step 2: Multiply By 25 (Then Reality-Check It)

Take each spending level and multiply by 25 for a rough target. For example:

- Budget FI: $40,000 x 25 = $1,000,000.

- Baseline FI: $80,000 x 25 = $2,000,000.

- Blockbuster FI: $250,000 x 25 = $6,250,000.

These numbers are not sacred. They’re a starting point. A strong pension, Social Security, or rental income may reduce how much you need invested. On the flip side, early retirement, high medical risks, or big family obligations may mean you need more cushion.

Step 3: Compare Your Passive Income To Those Targets

Now look at what your money is doing for you right now. How much income do you already generate from:

- Dividends and interest

- Rental properties

- Royalties or digital products

- Small businesses or side hustles that you could operate part-time or hands-off

If your current passive income already covers your Budget FI spending, congratulationsyou’re technically at Level 1. If it covers your current lifestyle with room for surprises, you’re closer to Level 2. If it does all that and then some, you’re flirting with Level 3.

Myths That Hold People Back From FI

When you read about FIRE online, it’s easy to think it’s only for Silicon Valley employees or six-figure power couples. Reality is more nuanced.

Myth 1: You Need A Massive Salary

Yes, high earners can get there faster, but countless stories show people building FI on middle incomes by combining high savings rates, smart investing, and a long-term mindset. Side hustles, career pivots, and geographic arbitrage (living in a cheaper area while earning higher wages) are powerful tools.

Myth 2: FI Means You Never Work Again

Financial independence doesn’t require you to stop working forever. It simply means money is no longer the primary driver of your decisions. Many financially independent people still workteaching, consulting, starting passion projects, or freelancingbecause they enjoy it and like the extra cushion.

Myth 3: You Must Choose Between Enjoying Life Now Or Later

The smartest FI plans make room for both. That might mean front-loading savings in your 20s and 30s to buy flexibility later, but still budgeting for occasional trips, hobbies, or experiences that make the journey worthwhile. Extreme deprivation rarely leads to long-term success; balance does.

Designing Your Own Path Through The Three Levels

So how do you turn this from a nice framework into a real-life plan?

1. Decide Which Level You Actually Want

Be honest with yourself. Are you genuinely happy with a lower-cost lifestyle if it means more time freedom earlier? Or will you feel constantly cramped unless you have Baseline or Blockbuster FI? There’s no wrong answerjust trade-offs.

2. Build A Simple, Aggressive-But-Realistic Plan

From there:

- Cut high-impact costs first: housing, transportation, and debt interest.

- Increase income where possible: upskill, change jobs, negotiate, or add side income.

- Automate saving and investing: treat investing as a non-negotiable bill you pay your future self.

- Use tax-advantaged accounts where it makes sense, and build taxable investments for flexibility.

3. Track Progress In FI “Levels,” Not Just Net Worth

Instead of obsessing over your exact net worth, track how many years of expenses your portfolio could support and which level’s lifestyle it currently matches. It’s more motivating to say “I’m already at Budget FI and halfway to Baseline FI” than “I still need another $600,000.”

Real-World Experiences With The Three Levels Of FI

Theory is helpful, but FI really comes alive when you look at how people actually live it. While details differ, certain patterns show up again and again.

From Burnout To Budget FI

Imagine a 31-year-old software engineer who has been grinding 60-hour weeks in a big city since graduation. After nearly a decade of saving aggressively, investing in low-cost index funds, and living with roommates long after friends “upgraded,” she reaches the point where her investments can cover a bare-bones lifestyle in a smaller city.

She doesn’t feel “rich.” But she does feel something powerful: options. She moves to a lower-cost area, picks up contract work only when she wants to, and spends more time on health, family, and creative projects. Money doesn’t disappear as a concern, but the constant fear of needing her job to survive fades. That’s Budget FI in actionimperfect, but life-changing.

Baseline FI With Kids And Trade-Offs

Now picture a couple in their early 40s with two kids. They’ve been intentional for years: saving 25–35% of their income, buying a modest house instead of the “forever home,” and investing heavily in index funds and a rental property. By their mid-40s, their portfolio and rental income can cover their current lifestyle.

On paper, they’re at Baseline FI. In practice, they still wrestle with decisions: Should one parent quit full-time work? Is it safe to step away while kids are still young and expenses are high? They opt for a middle path: one partner shifts to a more flexible part-time role while the other stays full-time but in a less stressful position. Their FI status doesn’t force them into a decision; it gives them more versions of a good life to choose from.

Blockbuster FI And The “Now What?” Question

At the top is the person who has truly hit Blockbuster FI. Maybe it’s a business owner who sold a company for several million dollars or a long-term executive who combined high income with disciplined investing and real estate.

They have more than enough to fund a luxurious lifestyle. Their passive income covers generous spending, and their kids’ education is paid for. Yet they still face deeply human questions: What projects are worth doing now that money isn’t the main motivator? How do they stay grounded and connected to others? What legacy do they want to leave?

Many in this bracket end up building passion businesses, mentoring younger professionals, or focusing heavily on philanthropy. They learn that at a certain point, money stops dramatically increasing happinessand purpose, health, and relationships do the heavy lifting.

Lessons From Across The Levels

Across all three levels, a few lessons repeat:

- Clarity beats vibes. Knowing your real spending, FI number, and target level pulls you out of vague anxiety and into concrete planning.

- Flexibility is a superpower. Being willing to adjust your lifestyle, work type, or location can dramatically reduce the amount you need for each level.

- Work can still matter. Many people discover they enjoy some kind of work even after reaching FIjust with healthier boundaries.

- It’s a spectrum, not a finish line. People move up and down levels over time as life changes. That’s not failure; that’s reality.

Ultimately, “The Three Levels Of Financial Independence” isn’t about bragging rightsit’s a framework to help you design a life where money supports your values instead of dictating them. Whether your goal is Budget, Baseline, or Blockbuster FI, each level offers something priceless: the freedom to choose.