Table of Contents >> Show >> Hide

- First, a quick reality check: “Yield” is not one thing

- The “menu” of high-yield savings options (with plain-English trade-offs)

- 1) High-yield savings accounts (HYSAs): the crowd favorite

- 2) Money market accounts (MMAs): a savings account with a few extra knobs

- 3) Money market funds (MMFs): higher yield potential, but different “safety” rules

- 4) Certificates of deposit (CDs): lock in a rate, trade flexibility for certainty

- 5) Brokered CDs: CD convenience inside a brokerage

- 6) U.S. Treasury bills (T-bills): short-term government-backed yield

- 7) Series I Savings Bonds: inflation protection with rules (and a little patience)

- 8) Cash management accounts and brokerage “sweeps”: convenience with fine print

- 9) Short-term bond funds/ETFs: more yield sometimes, but price can move

- How to choose: build a simple “cash stack” instead of chasing one perfect product

- Common pitfalls (aka how savers accidentally sabotage their own yield)

- Pitfall 1: Ignoring insurance limits and assuming “all accounts are automatically covered”

- Pitfall 2: Confusing look-alike names (money market account vs money market fund)

- Pitfall 3: Falling for “headline APY” while stepping on fees

- Pitfall 4: Locking everything up at once

- Pitfall 5: Forgetting taxes

- A simple “options galore” blueprint (steal this)

- Conclusion

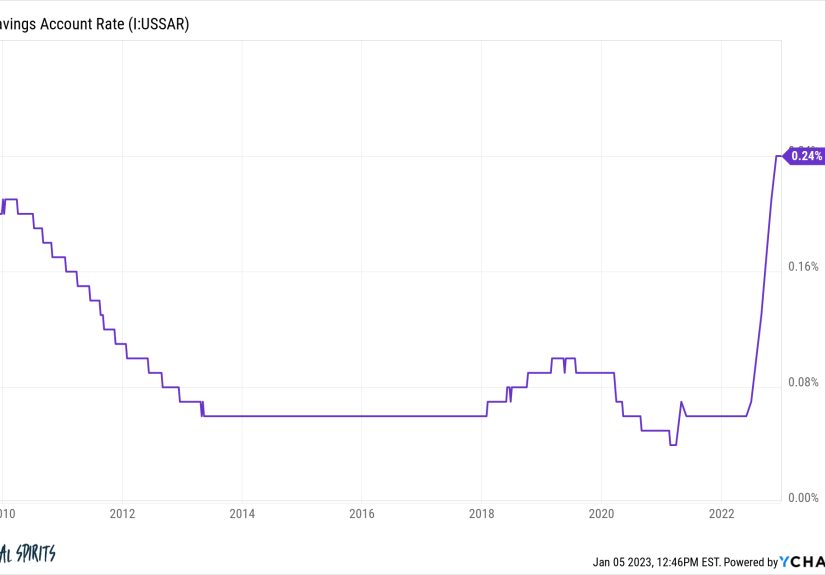

For years, “earning interest” on your savings was basically a punchline. You’d open a savings account, watch it earn about enough to buy one (1) gumdrop per year, and call it adulthood.

But the world changed. Today, if your money is just sitting in a low-interest account, it’s not “being safe”it’s quietly missing out on options that can pay meaningfully more while still keeping risk low.

The good news: you don’t need a finance degree, a Bloomberg terminal, or an emotional support spreadsheet. You just need to know what the main “cash and cash-like” choices are,

what trade-offs come with each one, and how to mix them so your savings can earn real yield without turning your life into a constant rate-chasing hobby.

First, a quick reality check: “Yield” is not one thing

When people say “yield on savings,” they usually mean the annual percentage yield (APY)the yearly return including compounding. But different products pay yield in different ways:

bank accounts pay interest, money market funds distribute income, Treasury bills “pay” by maturing at face value after you bought them at a discount, and savings bonds accrue interest you collect later.

Also: yields change. Banks adjust rates, money market fund yields move with short-term markets, and Treasuries reflect auction and market rates. So the goal isn’t to find the one perfect option forever

it’s to build a simple setup that stays competitive with minimal effort.

The “menu” of high-yield savings options (with plain-English trade-offs)

1) High-yield savings accounts (HYSAs): the crowd favorite

A high-yield savings account is typically an online savings account that pays a higher APY than many traditional brick-and-mortar banks. It’s still a bank deposit, usually FDIC-insured if the bank is FDIC-insured,

and your money stays liquid (meaning you can access it when you need it).

- Best for: emergency funds, “next 6–18 months” savings, and anyone who values simplicity.

- Watch for: variable APYs that can drop, minimum balance requirements, and occasional fees or transfer limits.

- Why it’s great: it’s basically “set it and forget it” yieldyour savings earns more without you doing anything fancy.

Example: If you keep $10,000 in a savings account earning 4% APY, you’d earn about $400 over a year (roughly). If that same $10,000 sits earning 0.01%,

that’s about $1. The difference is not “life-changing,” but it is “why would I donate $399 to the void?”

2) Money market accounts (MMAs): a savings account with a few extra knobs

A money market account is a bank deposit account (not a money market fund). Many MMAs offer higher interest than basic savings and sometimes include limited check-writing or a debit card.

If it’s a deposit account at an FDIC-insured bank, it’s generally FDIC-insured up to coverage limits.

- Best for: people who want a bit more access (like checks/debit) while still earning decent interest.

- Watch for: higher minimum balances, tiered rates (great rate only if you keep a large balance), and fees if you fall below the minimum.

3) Money market funds (MMFs): higher yield potential, but different “safety” rules

Money market funds are mutual funds that invest in short-term, high-quality debt instruments. They’re designed to be highly liquid and relatively low risk

but they are not bank deposits, and they are not FDIC-insured.

Many investors use government or Treasury money market funds as a “cash hub” in a brokerage account because yields can be competitive and you can often move money into investments quickly.

Just remember: “low risk” is not “no risk.” Money market funds can face stress in rare situations (the phrase “break the buck” exists for a reason).

- Best for: savers who use a brokerage, keep cash for near-term investing, or want competitive yield without locking money up.

- Watch for: not FDIC-insured, yield can change daily, and access depends on your brokerage’s settlement rules.

4) Certificates of deposit (CDs): lock in a rate, trade flexibility for certainty

CDs pay a fixed rate for a set term (like 6 months, 12 months, 24 months). They’re usually FDIC-insured (or NCUA-insured at credit unions) if held within coverage limits.

The big trade-off: if you need the money early, you may pay an early withdrawal penalty.

- Best for: money you won’t need for a known window of time, especially if you like predictable returns.

- Watch for: early withdrawal penalties (often measured in days/months of interest), and the “oops, rates went up and I’m locked in” regret.

- Pro tip: consider a CD ladder (spreading money across multiple maturities) to reduce timing risk.

CD ladder example: Instead of locking $12,000 into one 12-month CD, you could put $4,000 into a 3-month CD, $4,000 into a 6-month CD, and $4,000 into a 12-month CD.

Every few months, something maturesgiving you a chance to reinvest at current rates or use the cash if life happens.

5) Brokered CDs: CD convenience inside a brokerage

Brokered CDs are CDs you buy through a brokerage (instead of directly from a bank). They can offer access to rates from many banks in one place,

and (if issued by FDIC-insured banks and structured properly) they can be FDIC-insured within limits.

The trade-off is that selling before maturity can be different from “breaking” a bank CDrather than paying a fixed penalty, you may have to sell on the market,

and the price can be higher or lower depending on interest rates at that time. Translation: more flexibility sometimes, but not guaranteed to be painless.

6) U.S. Treasury bills (T-bills): short-term government-backed yield

Treasury bills are short-term U.S. government securities that typically mature in one year or less (common terms range from a few weeks up to 52 weeks).

You buy them at a discount, and at maturity you receive the face valuethe difference is your return.

- Best for: people who want very low credit risk, short terms, and potentially tax advantages at the state/local level.

- Watch for: reinvestment risk (when a bill matures, the new rate might be lower), and the “auction calendar” learning curve.

A popular approach is a T-bill ladder, where you buy multiple bills with staggered maturitiesso cash is regularly coming due and you can keep rolling it forward.

This can be a clean way to avoid locking everything up at one rate on one day.

7) Series I Savings Bonds: inflation protection with rules (and a little patience)

I bonds are U.S. savings bonds designed to protect against inflation. The rate changes every six months based on inflation measures, and the bond has a fixed-rate component

that stays with the bond for its life. There are purchase limits per calendar year, and there are important access rules.

- Best for: medium-term savings where inflation protection matters and you can leave the money alone.

- Watch for: you generally can’t redeem within the first 12 months, and redeeming before 5 years typically means forfeiting 3 months of interest.

- Tax note: savings bond interest is generally subject to federal tax but not state/local tax, and you can often defer federal tax until redemption.

8) Cash management accounts and brokerage “sweeps”: convenience with fine print

Many brokerages offer cash management features. Your uninvested cash might be placed into a “sweep” program that moves it into partner banks (often eligible for FDIC insurance up to limits),

or it may sit as a cash balance earning a lower rate unless you choose an alternative.

The key is to understand where your cash is actually parked. “Cash” in a brokerage can mean:

- Bank sweep deposits: typically FDIC-eligible (subject to limits) because the money is held at program banks.

- Money market fund holdings: not FDIC-insured (they’re securities), though brokerage protections like SIPC may apply in certain situations.

9) Short-term bond funds/ETFs: more yield sometimes, but price can move

Short-term bond funds and ETFs can offer higher yield than bank deposits in some environments, but they introduce market risk.

Bond prices and interest rates tend to move in opposite directionsso if rates rise, bond prices often fall.

- Best for: money you truly don’t need on a specific date, and savers comfortable with small price swings.

- Watch for: price volatility, interest rate risk, and the temptation to treat it like a savings account (it isn’t).

How to choose: build a simple “cash stack” instead of chasing one perfect product

Here’s a practical way to organize savings so you get higher yield without sacrificing sleep:

Step 1: Keep your true emergency fund boring and liquid

Emergency money needs to be there when you need it, not when your CD matures or when the market feels cooperative.

A HYSA or an insured money market account is often the cleanest home for 3–6 months of essential expenses.

Step 2: Put “scheduled spending” on a predictable timeline

If you know you’ll need money in 3, 6, 9, or 12 months (tuition, a car, a move, a tax bill), consider a CD ladder or T-bill ladder.

You can match maturities to your timeline so you don’t have to guess.

Step 3: Park “patient cash” where it can earn without locking you in forever

For savings you likely won’t touch for at least a year, I bonds can be compelling (if you accept the access rules),

and money market funds in a brokerage can be a strong “cash hub” if you like keeping everything in one place.

Common pitfalls (aka how savers accidentally sabotage their own yield)

Pitfall 1: Ignoring insurance limits and assuming “all accounts are automatically covered”

FDIC insurance generally covers up to $250,000 per depositor, per FDIC-insured bank, per ownership category. Credit unions have similar coverage through NCUA for federally insured credit unions.

If your balances get large, spreading deposits across ownership categories or institutions can matter.

Pitfall 2: Confusing look-alike names (money market account vs money market fund)

A money market account is a deposit account (often insured if held at an insured institution).

A money market fund is an investment product (not FDIC-insured) that aims for stability but can carry risks.

The names sound like twins; the protections are not.

Pitfall 3: Falling for “headline APY” while stepping on fees

A strong APY is greatuntil a monthly fee, minimum balance requirement, or rate tiering eats the benefit.

Always check the rules: fees, minimums, how often rates change, and what actions are required to earn the advertised yield.

Pitfall 4: Locking everything up at once

If you put all your cash into a long CD today, you’ve made one big bet on today’s rate being “the right one.”

Ladders help you avoid rate regret by giving you multiple chances to reset.

Pitfall 5: Forgetting taxes

Interest is usually taxable. Treasuries are generally exempt from state and local income taxes (though still federally taxed),

and savings bond interest is generally federally taxable but not state/localand can often be deferred until redemption.

Taxes shouldn’t be the only factor, but they’re not nothing either.

A simple “options galore” blueprint (steal this)

If you want a straightforward setup that covers most real-life needs, try this structure:

- Everyday buffer: checking account (for bills and normal spending).

- Emergency fund: HYSA or insured money market account (liquid + competitive yield).

- Near-term goals (3–12 months): T-bill ladder or CD ladder matched to your dates.

- Inflation hedge (money you can leave alone): I bonds (within purchase limits and rules).

- Brokerage cash hub (optional): government/Treasury money market fund for flexible cash.

This isn’t about maximizing every last basis point. It’s about getting most of the available yield with minimal complexity.

If your system is so complicated you need a whiteboard and three cups of coffee to move $500, you’ll stop using it. And then your yield goes back to gumdrop levels.

Conclusion

You really do have options galore for yield on your savingsmore than most people realize. The “best” choice depends on what the money is for:

immediate access (HYSAs/MMAs), scheduled spending (CDs/T-bills), inflation protection (I bonds), or flexible brokerage cash (money market funds and sweeps).

If you take only one thing away: match the tool to the timeline, understand the protection (FDIC/NCUA vs investment risk), and use ladders to avoid locking everything up at once.

You don’t need to chase every rate. You just need to stop letting your savings earn “proudly negligible” interest.

General info only, not financial advice. If you’re under 18, involve a parent/guardian for account setup and decisions.

Real-World Experiences: on What Savers Actually Run Into

The first “aha” moment for many savers is embarrassingly simple: they finally look at their bank statement and realize their longtime savings account paid, like, $2.13 in interest for an entire year.

That’s not a “return.” That’s a tip jar. Once people notice, the next experience is usually a burst of motivationopening a high-yield savings account feels like discovering a hidden level in a video game

where your coins suddenly start multiplying.

A common story: someone moves their emergency fund to a HYSA and, for the first few months, checks it like it’s a new pet. “Look! It earned interest again!”

Then reality kicks in: the APY changes. That’s when people learn the difference between a fixed rate and a variable APY. It’s not betrayalit’s how these accounts work.

The practical takeaway most savers land on is: don’t panic over small moves. If a bank becomes consistently uncompetitive, shop aroundbut don’t treat your savings like a day-trading account.

Another real experience is the “I locked it up and now I need it” moment. This happens with CDs. The rate looked great, the term felt reasonable, and then life happened:

car repairs, surprise travel, a medical bill, or just “I forgot property taxes are a real thing.” Paying an early withdrawal penalty feels like a slap on the wrist from your past self.

People who go through this once often become ladder fans. After that, they spread money across multiple maturities so there’s always a release valve.

Brokerage cash can be its own learning curve. Many savers assume uninvested cash in a brokerage automatically earns a high rate, then discover it might be sitting in a low-paying default option.

The “aha” here is that you sometimes have to choose your cash vehiclelike selecting the right parking spot instead of leaving your car running at the curb.

Once people switch to a government money market fund or confirm a sweep program, they often feel like their financial life got cleaner: one dashboard, fewer logins, and cash earning more.

I bonds tend to create a different kind of experience: patience. Savers like the inflation protection, but the 12-month minimum holding period forces a mindset shift.

People who treat I bonds as “emergency money” get frustrated; people who treat them as “medium-term, don’t-touch-it savings” love them.

The best “real world” lesson is that yield isn’t just a numberit’s a contract with time. When you match the product to your timeline, saving stops feeling like punishment

and starts feeling like progress you can actually measure.