Table of Contents >> Show >> Hide

- The Passive vs. Active Story We Tell (And Oversimplify)

- What the Scorecards Really Say About Active Performance

- Why Most Active Funds Still Struggle

- How to Look for the Right Kind of Active Fund

- Blending Active and Passive: A Common-Sense Framework

- Common Mistakes Investors Make With Active Funds

- Experiences and Lessons From the Real World

- Conclusion: A Smarter Way to Think About Active Funds

If you spend any time in the personal finance corners of the internet, you’ve probably heard a very confident claim:

“All active funds underperform the index. Just buy the S&P 500 and call it a day.”

There’s a lot of truth baked into that sentence. Decades of research and the well-known SPIVA scorecards show that

most actively managed funds fail to beat simple low-cost index funds over long periods, especially in U.S. large-cap stocks.

But “most” is not the same as “all,” and “over long periods” leaves some room for nuance.

The original “Not All Active Funds Consistently Underperform” argument, popularized by Ben Carlson on his blog

A Wealth of Common Sense, zoomed in on one very interesting corner of the market:

intermediate-term bond funds. In that niche, a majority of active funds have historically beaten their

benchmarkat least over certain periods.

That little wrinkle forces us to upgrade our investing rule of thumb from “never use active funds” to something

more realistic and more useful.

In other words, this isn’t an argument for throwing all your money at the latest hot mutual fund. It’s an argument

for common sense: understanding where active management tends to fail, where it occasionally shines,

and how a thoughtful investor can combine passive and active strategies without losing their shirtor their sanity.

The Passive vs. Active Story We Tell (And Oversimplify)

The basic passive-investing pitch is simple: markets are hard to beat, costs matter, and index funds are cheap,

diversified, and boring in exactly the right way. Study after study, including SPIVA’s long-running reports and

Morningstar’s active–passive scorecards, shows that a large majority of active equity funds underperform comparable

index funds once you account for fees, taxes, and survivorship (the fact that losers quietly disappear from the data).

Over 10-, 15-, or 20-year horizons, it’s common to see statistics like “80–90% of active funds underperform their

benchmark.”

That’s where the blanket advice comes from: if the odds of picking a long-term winner are that low, why bother?

But those headline numbers hide three important details:

- They vary by asset class (U.S. large-cap stocks, small caps, bonds, international stocks, etc.).

- They depend on the time period and market environment (booming bull markets are rough on active stock pickers).

- They say very little about how active funds outperform when they doand what risks they take to get there.

Once you look beyond the soundbites, you find pockets where active management has historically done better

especially in fixed income and some less efficient corners of the market.

What the Scorecards Really Say About Active Performance

The Long-Run Odds Are Still Tough for Stock Pickers

Let’s be clear up front: for broad U.S. equity categories, long-term odds still favor passive index funds.

SPIVA’s U.S. scorecards routinely show that a majority of actively managed large-cap funds lag the S&P 500 over

5-, 10-, and 15-year periods.

Recent data suggests that around half of large-cap managers underperformed over the most recent one-year period,

and a much higher percentage lagged when you stretch the horizon to a decade or more.

Persistence is another problem. Funds that outperform in one period rarely stay in the top tier over the next

few years. Studies from S&P Dow Jones and independent researchers consistently find that yesterday’s stars tend

to regress toward the meanor worse.

So if your plan is “I’ll just find the five-star manager who crushed it last year and ride that wave,” the data

is not on your side.

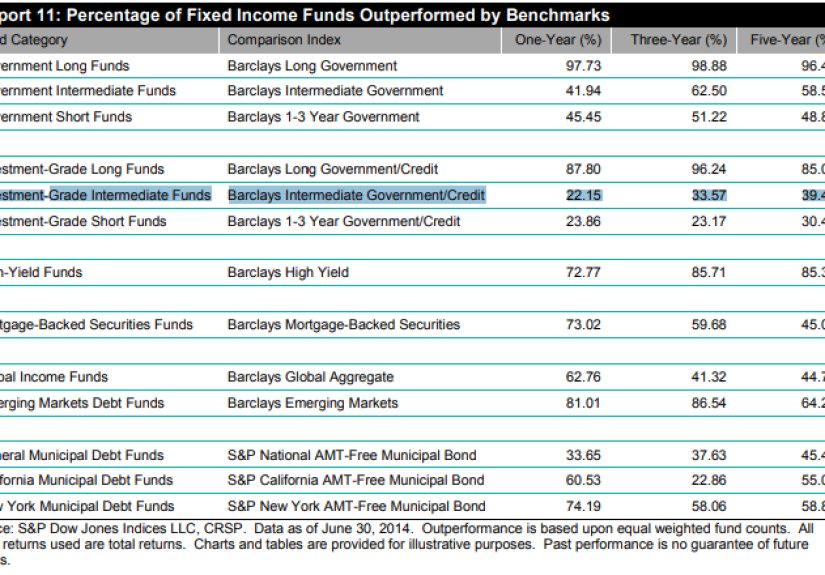

The Bond Market: An Awkward Exception

Now we get to the twist. In the SPIVA scorecard that Ben Carlson highlighted, intermediate-term bond funds showed

a very different pattern: over certain three- and five-year windows, a majority of active bond funds

outperformed their benchmark.

That’s the opposite of what we typically see in U.S. stocks.

Why? A few key reasons come up again and again:

-

The main bond benchmark (like the Bloomberg U.S. Aggregate Bond Index) tends to be heavy in government bonds,

which are safer but offer lower yields than corporate or mortgage-backed bonds. -

Many active funds take on a bit more credit risk (more corporates and securitized bonds) or tweak

their duration (interest-rate sensitivity). In a falling-rate environment, that has historically boosted returns. -

The bond market is larger and often less liquid than the stock market, so having a big, sophisticated trading

operation can occasionally be a genuine advantage.

In plain English: a lot of “outperformance” in bond funds comes from taking sensible (and sometimes not-so-sensible)

extra risks that the benchmark doesn’t takemore credit, different sectors, slightly longer duration, and so on.

The returns are real, but they’re not magic; they’re a trade-off between risk and reward.

Why Most Active Funds Still Struggle

If it’s possible for active funds to win, why do so many still lose? A few structural reasons keep showing up in

academic research and industry data.

Fees and Frictional Costs

Active funds have to pay portfolio managers, analysts, traders, and everyone else behind the curtain. That shows up

as higher expense ratios and, sometimes, performance fees. Several studies find that high-fee funds tend to deliver

lower net risk-adjusted returns than their cheaper peers.

Think of it this way: even if a manager matches the index before fees, a 1% annual fee means they’re

1 percentage point behind after costs. In competitive, relatively efficient markets, that fee drag is brutal.

Size and the “Too Much Money” Problem

Success creates a strange curse for active funds: once they post a strong track record, investors pile in, assets

balloon, and it gets harder to move quickly or exploit smaller mispricings. Research on fund size consistently

finds that very large funds often see their edge erode as they scale up.

In the stock world, this can mean owning more and more of the benchmark itself, which quietly pushes a once

differentiated strategy closer to “closet indexing.”

BehaviorOn Both Sides of the Table

Investors don’t buy and hold perfectly; they chase what just worked. Flows into mutual funds tend to follow recent

performance, which means many people buy after a good run and sell after a slump. That behavior can turn even a

decent active fund into a bad experience at the individual investor level.

Managers, for their part, face career risk: it’s hard to stick with an unpopular strategy when a couple of bad

years could get you fired. That pressure can nudge funds toward the benchmark and away from the bold decisions

that would be required to justify higher fees.

How to Look for the Right Kind of Active Fund

“Not all active funds underperform” is an observation, not an investment plan. To turn it into something you can

actually use, you need a process for identifying which active funds might deserve a place in your

portfolio.

1. Start With the Role in Your Portfolio

Before you even look at tickers, ask: “What job am I hiring this fund to do?” Common roles include:

- Core stock exposure (U.S. large-cap, total market)

- Satellite “tilts” (small-cap value, quality, specific sectors)

- Defensive ballast (high-quality bonds, absolute-return strategies)

- Specialized exposure (emerging markets, niche credit, etc.)

For broad core holdings, low-cost index funds usually remain the default. For more specialized or less efficient

asset classes, a carefully chosen active fund might be worth considering.

2. Prioritize Low Fees and Clear Differentiation

Look for funds with:

- Reasonable expense ratios relative to peers.

-

High “active share” – meaning the portfolio genuinely looks different from the benchmark, rather than holding the

same stocks in slightly different weights. Research suggests that, among active funds, those with higher active

share and lower costs have better odds of adding value. - A clearly articulated process the managers have stuck with across cycles.

If you’re paying for active management, you want actual active management, not a closet index fund with

a premium price tag.

3. Consider Where Active Has a Fighting Chance

Historical scorecards and industry reports suggest that active management has a better shot in:

- Certain bond categories, especially intermediate-term and niche credit strategies.

- Smaller-cap equities and some international markets that may be less efficiently priced.

- Strategies that exploit structural constraints (e.g., avoiding forced sellers, navigating illiquid corners of the market).

None of this guarantees success, but it can help you focus your due diligence where the long-term data isn’t quite

as stacked against you.

Blending Active and Passive: A Common-Sense Framework

One of the more practical takeaways from the “Not All Active Funds Consistently Underperform” discussion is that

you don’t have to choose sides in the active vs. passive debate. You can build a portfolio where index funds

do the heavy lifting, and carefully selected active funds fill in specific gaps.

A popular approach among advisors is a core–satellite structure:

- The core is built from low-cost index funds or ETFs (e.g., total U.S. stock, international stock, core bonds).

- The satellites are active or factor-based strategies targeting specific opportunities: a skilled bond manager,

a small-cap value strategy, or a flexible global fund.

In the bond context, Carlson highlighted a simple version of this idea: you can keep a big chunk of your fixed-income

allocation in a broad, mostly government-heavy index fund, then selectively add active managers who tilt toward

credit or other bond sectors to improve yield and diversificationif that fits your risk tolerance.

The key is intentionality. You’re not buying active funds because a commercial told you to or because last year’s

return chart looked exciting. You’re using them as tools to solve specific problems that broad index exposure

doesn’t address quite as well.

Common Mistakes Investors Make With Active Funds

Even if you accept that not all active funds are doomed, there are plenty of ways to misuse them. Here are some

errors to avoid:

Chasing Recent Winners

Performance-chasing is the classic blunder. Persistence studies show that funds in the top quartile over one

period rarely stay there over the next few years.

If your main selection criterion is “whatever did best in the last three years,” you’re effectively buying high

and setting yourself up to sell low.

Ignoring the Benchmark and Risk Profile

Many investors don’t realize how different their active fund is from the index it’s compared to. An intermediate

bond fund that looks like a safe “core” holding might actually carry much more credit risk than the benchmark.

That can feel great in calm markets and very unpleasant during stress.

Always look under the hood: sector weights, credit quality, duration, geographic exposure, and concentration in

top holdings.

Over-Diversifying the Active Part

Buying five or six large-cap active funds that all hug the same benchmark mostly adds fees, not diversification.

If you’re going to use active strategies, each one should have a clearly different style, process, or asset class

focus.

Forgetting About Taxes

High-turnover strategies can create bigger tax bills via realized capital gains. Index funds tend to be very

tax-efficient; some active funds, not so much. If you’re investing in a taxable account, after-tax returns matter

more than the pre-tax numbers in the glossy marketing deck.

Experiences and Lessons From the Real World

Theory is nice, but active vs. passive gets real when it hits someone’s actual portfolio. To bring the “Not All

Active Funds Consistently Underperform” idea down to earth, imagine three different investors and how this plays

out for each of them.

Case 1: The All-Active Investor Who Got Tired

Sarah started investing in the early 2000s. She loved reading fund rankings and manager profiles, and she built a

portfolio entirely out of actively managed stock funds. Some of them did brilliantly for a while; others lagged.

Over 15–20 years, her overall performance was… fine, but nothing special once she accounted for fees and the fact

that she always seemed to buy into a star fund after a big run.

After finally comparing her results with a simple blended index portfolio, she realized she had taken more risk,

paid more in fees, and spent far more time worrying than she needed to. Her response was not to swear off active

funds forever, but to flip the structure: she moved most of her money into a small set of diversified index ETFs

and kept just one or two active funds in areas where she believed they had an edge (a specialized bond fund and

a global small-cap strategy).

Her returns didn’t suddenly explode upwardbut her stress level dropped, and her portfolio became easier to manage

and understand. That’s the “common sense” part in action.

Case 2: The Index Investor Who Ignored Bonds

Mark, on the other hand, took the “all active funds are bad” mantra to heart. He built a portfolio entirely from

cheap, broad index funds: total U.S. stock, total international, and a total bond market index.

For equity, this made perfect sense. But after reading more about how many intermediate-term bond funds had

historically beaten their benchmarks by taking controlled amounts of extra credit and sector risk, he realized his

bond sleeve might be leaving something on the table.

He didn’t blow up his plan or start day-trading bond funds. Instead, he carved out a modest portionsay 20–30% of

his fixed-income allocationfor a low-cost active bond strategy with a clear mandate and long record. The rest

stayed in the plain-vanilla index.

Over time, the difference in returns wasn’t dramatic year to year, but the active sleeve did add a bit of extra

yield and diversification. More importantly, Mark now understood exactly why that fund behaved differently

during rate shocks or credit scares, so he wasn’t surprised when it zigged while his index bond ETF zagged.

Case 3: The “Barbell of Effort” Investor

Finally, there’s Dana, who runs her portfolio on a “barbell of effort” principle. On one side of the barbell, she

holds boring, low-cost index funds that require almost no ongoing decision-making. On the other, she allocates a

small, clearly defined slice of her money (maybe 10–15%) to a handful of active strategies where she’s willing to

put in serious work:

- Reading manager letters and understanding the strategy.

- Checking that fees stay reasonable and assets don’t balloon into the danger zone.

- Accepting multi-year stretches of underperformance without panickingif the thesis remains intact.

Dana’s experience highlights a subtle point: for active funds to pay off, you not only need the right managers,

you also need the right investor behavior. If you bail out at the first bad year, even the best

active strategy can’t help you.

Across all three stories, the pattern is the same:

- Passive investing provides a powerful, low-cost foundation.

- Active funds are tools, not trophiesyou use them where they make sense, not everywhere.

- Understanding your risk, your time horizon, and your own behavior matters as much as manager skill.

That’s the deeper lesson behind “Not All Active Funds Consistently Underperform.” The point isn’t to declare a

surprise victory for active managers; it’s to remind investors that good rules of thumb still have exceptions, and

that smart investing lives in the space between simple slogans and messy reality.

Conclusion: A Smarter Way to Think About Active Funds

The data is clear: most active funds, especially in U.S. large-cap stocks, fail to beat their

benchmarks over long periods. Costs, competition, and human behavior all conspire to make indexing the default

recommendation for the majority of investors.

But it’s equally true that not all active funds underperform all the time. Certain bond categories,

some smaller or less efficient markets, and a subset of differentiated, reasonably priced strategies have

historically added valuesometimes modestly, sometimes meaningfully.

A wealth of common sense suggests a middle path:

- Let low-cost index funds handle the bulk of your long-term wealth building.

- Use active funds selectively, where the structure of the market or the design of the benchmark creates room

for intelligent risk-taking. - Stay laser-focused on fees, risk, behavior, and the actual role each fund plays in your plan.

In the end, the question isn’t “active or passive?” It’s “What mix of tools gives me the highest odds of reaching

my goals, with risks I truly understand?” Once you start thinking that way, you’ve already moved beyond slogans

and into real investing.