Table of Contents >> Show >> Hide

- What Is a Price-Insensitive Buyer?

- Why They Show Up Near Peaks

- How This Looked at Prior Market Peaks

- What Makes These Buyers So Important

- Warning Signs That Price Sensitivity Is Fading

- What Usually Happens After the Peak

- What Investors and Buyers Should Learn

- Experience and Practical Perspective: What This Feels Like in Real Life

- Conclusion

- SEO Tags

Every market peak has a signature character. Sometimes it is the swaggering day trader. Sometimes it is the panicked homebuyer waiving inspections like they are pesky party invitations. And sometimes it is the perfectly respectable investor who says, “Yes, this looks expensive, but what if it gets even more expensive tomorrow?”

That person is the price-insensitive buyer. Not irrational in every case. Not reckless by definition. But at prior market peaks, this buyer often becomes the market’s final fuel source. When enough people stop asking, “What is this worth?” and start asking, “How fast can I get in?” prices can detach from old anchors like cash flow, replacement cost, rent, earnings, or plain old common sense.

This pattern has shown up again and again in stocks, housing, and speculative assets. Different decade, different haircut, same movie. The assets change. The playlist changes. The psychology barely does.

What Is a Price-Insensitive Buyer?

A price-insensitive buyer is someone whose willingness to purchase is driven less by valuation and more by access, urgency, narrative, or fear of missing out. In plain English, they are buying because they want exposure now, even if the sticker price looks stretched.

That does not always mean the buyer is foolish. A cash-rich household may care more about locking in a school district than haggling over the last 3%. A passive fund may buy because money is flowing in and it must allocate capital. A late-cycle investor may believe a powerful trend still has room to run. But at prior market peaks, the common thread is this: price discipline weakens right when prices are already elevated.

Once that happens, markets can rise faster than fundamentals. The marginal buyer is no longer debating value. The marginal buyer is chasing participation.

Why They Show Up Near Peaks

Price-insensitive buyers rarely dominate at the beginning of a cycle. Early buyers usually need a thesis. They need courage. They need spreadsheets. Late buyers need a story that sounds obvious.

By the time a market nears a peak, several forces tend to work together:

1. Recent gains feel like proof

When prices rise for long enough, many buyers stop seeing gains as a possibility and start treating them as a personality trait of the asset. Housing “always goes up.” The hot stock “always finds buyers.” The new technology “changes everything.” That is usually when the market starts charging extra for confidence.

2. Social proof becomes overpowering

People are not spreadsheets with shoes. If friends, coworkers, neighbors, podcasts, and timelines are all celebrating easy money, resisting the crowd becomes emotionally expensive. Watching everyone else get rich can make prudence feel like failure.

3. Liquidity hides risk

Easy credit, abundant cash, stimulus, or booming portfolio values can make buyers less sensitive to price. When money feels plentiful, valuation standards often get softer. It is amazing how “discipline” can become “maybe later” when asset values are moonwalking upward.

4. Narratives overpower metrics

At peaks, traditional measures still exist. They are just politely escorted out of the room. Earnings multiples, cap rates, rent yields, and affordability ratios get replaced by magical phrases like “new paradigm,” “must own,” and “you can’t time innovation.” Those phrases are not always wrong. They are just suspiciously popular right before drawdowns.

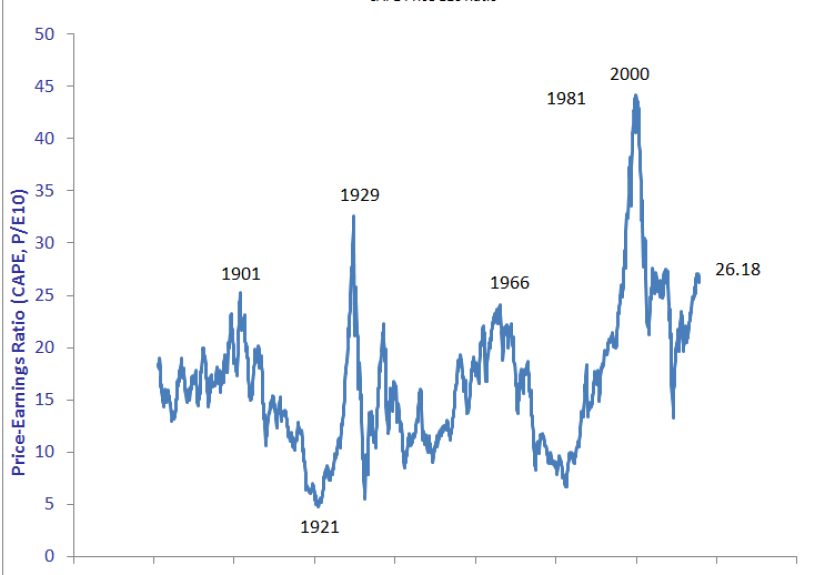

How This Looked at Prior Market Peaks

The Dot-Com Era: Clicks Before Cash Flow

During the late 1990s technology boom, investors poured money into internet and telecom names with extraordinary enthusiasm. The dominant logic was not always that profits were near. It was that the future would be so huge that today’s price would look quaint later. That belief attracted more buyers, which pushed prices higher, which validated the belief. It was a loop with excellent marketing and questionable brakes.

At a peak like that, price-insensitive buyers often emerge in waves. First come believers. Then come momentum traders. Then come newcomers who are less interested in intrinsic value than in the possibility of telling friends they got in before the next doubling. By the end, many buyers are effectively paying for a resale option: they believe someone else will buy from them later at an even higher price.

That is the subtle danger. Once the pool of “someone else” stops expanding, the market has to reconnect with math. Math is useful, but it has terrible bedside manner.

The Housing Bubble: When Homes Became Trading Chips

The mid-2000s housing boom offered a different version of price insensitivity. Here, the late-cycle buyer was often pulled in by easy credit, rising comps, speculative optimism, and the belief that waiting was riskier than overpaying. In many markets, buyers were no longer simply choosing a place to live. They were purchasing an expectation of future appreciation.

That shift matters. When an asset is bought mainly for use, buyers tend to care deeply about monthly affordability and long-term utility. When an asset is bought for expected resale gains, the willingness to stretch can rise dramatically. The market becomes more fragile because it depends on confidence, not just shelter demand.

Research on housing bubbles has repeatedly shown that speculative and short-horizon participants can amplify both prices and transaction volume. In other words, the market can get busier and more expensive at the same time for reasons that have less to do with fundamentals and more to do with momentum. That is usually not a calm, healthy sign. That is the sound of everyone trying to squeeze through the same doorway while insisting the room is getting bigger.

The Pandemic Boom and 2021 Mania: Stocks, Crypto, and Houses All at Once

More recent episodes showed how quickly price-insensitive behavior can spread across asset classes. In housing, bidding wars became common, homes sold above asking, investors bought a record share of homes in parts of 2021, and cash buyers held unusual power. In equities, meme-stock surges showed how social media, options activity, and identity-driven investing could accelerate buying even when business fundamentals were shaky.

Here the late-cycle buyer was not always rich or institutionally sophisticated. Sometimes it was the opposite: first-time participants, newly energized by apps, communities, and viral narratives. Buying became frictionless. Commentary became entertainment. The line between conviction and adrenaline got blurry.

The mechanics differed by market, but the emotional rhythm was familiar. Rising prices created headlines. Headlines created attention. Attention created more buying. And that buying increasingly came from participants who were less focused on valuation than on not being left behind.

What Makes These Buyers So Important

At a market peak, the price-insensitive buyer is not just another buyer. They are often the marginal buyer, the person whose willingness to pay a little more sets the next benchmark for everyone else. This matters because markets are made at the margin, not by the average opinion of every participant.

If the marginal buyer is cautious, prices stall. If the marginal buyer is euphoric, prices can overshoot. That is how a handful of aggressive bids in a neighborhood can reset comparable sales. That is how concentrated buying into a narrow set of glamour stocks can distort an index. That is how assets begin to look “supported” right up until support turns out to be mostly vibes.

Passive flows can add another twist. When money pours into index products, the largest winners can receive even more demand simply because they are already large. This can reinforce momentum and make the most expensive names feel unstoppable. It can also make a peak look healthier than it is because index strength may hide weak breadth under the surface.

Warning Signs That Price Sensitivity Is Fading

Buyers waive protections

In housing, inspection waivers, appraisal-gap promises, and all-cash bids can signal that winning matters more than price discipline. In financial markets, the equivalent may be leverage, options chasing, or ignoring basic downside scenarios.

Narrative outruns valuation

When “this time is different” becomes a mainstream argument, caution is warranted. Sometimes this time really does include meaningful innovation. It still does not repeal arithmetic.

New entrants arrive late and fast

Late-stage booms often attract novice or shorter-horizon participants. That can make prices more unstable because these buyers may be less anchored to fair value and more reactive to sudden reversals.

Market leadership gets narrow

When only a small cluster of names or neighborhoods carries the market higher, enthusiasm can look broad even when it is concentrated. Peaks often wear a very flattering mask.

Everyone has a reason to ignore the price

The homeowner says rates may fall later. The trader says momentum is still intact. The fund says inflows must be invested. The optimist says the old metrics no longer apply. When every participant has a different excuse for paying up, the result can look suspiciously coordinated.

What Usually Happens After the Peak

Once price-insensitive demand cools, markets do not need a dramatic villain. They just need fewer urgent buyers. That is often enough.

The first shift is subtle. Bids come in lower. Volume softens. Listings take longer. The “can’t lose” trade becomes a “let’s wait and see” trade. Then the air pocket appears. Prices that rose on confidence alone have trouble staying elevated when confidence becomes selective.

Importantly, the unwind does not always look like an instant crash. Sometimes it is a long plateau where returns go nowhere while fundamentals slowly catch up. Sometimes it is a violent drop. Sometimes it is a rolling correction in the hottest segments first. But in nearly every case, the buyer who ignored price near the top learns the same expensive lesson: a great story and a good entry point are not the same thing.

What Investors and Buyers Should Learn

The lesson is not “never buy expensive assets.” Some assets stay expensive for good reasons. The lesson is to notice when your own behavior becomes less about value and more about social pressure, urgency, or envy dressed in professional clothing.

Ask better questions. What cash flow, rent, earnings power, or strategic value justifies this price? What assumptions must remain true for the purchase to work? If the asset falls 20%, am I still comfortable owning it? Am I buying because the thesis is strong, or because other people already made money?

That last question is the sneakiest one. Markets are very good at making borrowed confidence feel original.

Peak behavior often looks intelligent in real time because it is reinforced by recent winners. But history suggests that when buyers become notably insensitive to price, the easy upside is often behind them, not ahead of them. By the time the crowd stops negotiating, risk has usually started negotiating back.

Experience and Practical Perspective: What This Feels Like in Real Life

Talk to people who bought near prior peaks, and the experience is rarely described in the cold language of valuation. It is emotional. It feels urgent. The market starts to seem like a train leaving the station, and the only unacceptable outcome is being left on the platform holding a coffee and a sensible opinion.

In housing, buyers often describe the process as exhausting and strangely numbing. At first they compare neighborhoods, mortgage costs, renovation budgets, and long-term plans. After losing several bidding wars, the decision process changes. Winning becomes the goal. Price becomes a secondary detail. A buyer who once would have argued over $15,000 suddenly agrees to pay far above list, skip repairs, cover an appraisal gap, and tell themselves it is all fine because “everyone is doing it.” That is price insensitivity in sneakers.

In stocks, the same emotional shift can happen on a phone screen in under ten minutes. An investor watches a name rise 20%, then 40%, then trend all over social media. Friends are discussing gains. Commentators are inventing grand theories. Soon the investor is not evaluating the company so much as negotiating with regret. The internal monologue changes from “Is this worth buying?” to “Can I stand watching this go higher without me?” That is how discipline gets replaced by speed.

One of the most common experiences at prior peaks is the illusion of safety created by a crowd. People assume that because many others are doing the same thing, the decision must be less risky. In practice, the opposite can be true. When everyone is leaning the same way, the market can become fragile. All it takes is a small disappointment, a rate shock, a weaker earnings report, a funding issue, or a shift in sentiment, and suddenly the crowd that felt reassuring becomes the exit line.

Another recurring experience is rationalization. Buyers near peaks are often highly articulate. They can produce excellent reasons for paying too much. Maybe rates will come down. Maybe artificial intelligence changes every valuation framework. Maybe this city will never cool off. Maybe the short squeeze is just starting. Maybe the crypto token is “building community.” The human mind is brilliant at constructing elegant arguments after emotion has already made the decision.

Then comes the aftertaste. Sometimes it is immediate. Sometimes it takes months. The buyer looks back and realizes they were not really acting on deep conviction. They were reacting to velocity. They were buying movement, not value. That realization is uncomfortable, but it is also useful. It teaches a practical lesson that spreadsheets alone often cannot: markets are not only pricing mechanisms; they are emotional amplifiers.

The healthiest takeaway is not cynicism. It is self-awareness. Everyone is vulnerable to peak psychology. The trick is not to pretend immunity. The trick is to build guardrails before the excitement starts. Set a valuation range. Define a maximum bid. Decide in advance what conditions would make you walk away. Give future-you a rule, because peak-you may suddenly become a poet of bad decisions.

That is the real experience behind price-insensitive buying at prior market peaks. It does not feel reckless in the moment. It feels reasonable, urgent, and socially validated. Which is exactly why it keeps happening.