Table of Contents >> Show >> Hide

- What “tactical equity” actually means (in human language)

- Why the “case for tactical” keeps coming back

- Setting the right expectations (or: how to avoid being angry at math)

- What part of the portfolio can tactical risk management replace?

- Whipsaws, drawdowns, and the emotional math of risk

- Why diversification of signals matters as much as diversification of holdings

- Concrete examples of tactical equity frameworks

- Implementation realities: fees, taxes, turnover, and the “looks easy” trap

- A practical way to decide if tactical equity belongs in your plan

- Conclusion: Tactical equity as a toolnot a personality

- Real-World Experiences (Composite Examples) With Tactical Equity

- SEO Tags

“Tactical equity” is one of those phrases that can make reasonable people reach for the mute button.

It sounds like a glossy brochure, a late-night infomercial, or a cousin of “one weird trick” investing.

And yet, in the Talk Your Book episode featured on A Wealth of Common Sense, the conversation lands in a much more grounded place:

tactical strategies aren’t magicthey’re rules. And rules can be useful when markets get loud, your emotions get louder, and your investing plan starts

to look suspiciously like a napkin you once scribbled on in 2017.

The episode (with Corey Hoffstein of Newfound Research) frames tactical equity the way it should be framed: not as “market timing to get rich,” but as

risk managementa systematic attempt to reduce the damage from deep, prolonged drawdowns while keeping meaningful exposure to the equity risk premium.

Done well, it can be a portfolio tool. Done poorly, it becomes an expensive way to underperform while feeling very busy about it.

What “tactical equity” actually means (in human language)

In plain English, a tactical equity approach tries to answer one question:

How much equity risk should I take right now, given what markets are doingnot what I hope they’ll do?

It typically uses quantitative signalsoften based on trend, momentum, and sometimes volatilityto scale exposure up or down.

The key word is “systematic.” Tactical investing is not supposed to be “I feel a crash coming because my barber is bullish.”

It’s more like: “If the market is behaving like it’s in a sustained downtrend, we reduce risk; if it’s behaving like it’s in a sustained uptrend, we add risk.”

That’s a very different pitch than prediction. And it’s the difference between a seatbelt and a crystal ball.

Common building blocks

- Trend filters (e.g., moving-average rules) to avoid major downtrends.

- Momentum (relative or absolute) to tilt toward what’s working and away from what’s not.

- Defensive assets (cash, T-bills, short/intermediate Treasuries) as “parking spots” when risk looks ugly.

- Position sizing (sometimes volatility targeting) to avoid going from 100% stocks to 0% stocks overnight.

Why the “case for tactical” keeps coming back

Tactical strategies are perennial because they speak to a real pain:

investors don’t mind volatility; they mind regret. A normal bear market is one thing.

A drawdown that changes your retirement timeline is another.

Tactical equity’s promisewhen stated honestlyis not “you’ll beat the market every year.”

It’s more like: “We may sacrifice some upside in exchange for potentially smaller and/or shorter drawdowns.”

That trade-off isn’t automatically good or bad. It depends on your objectives, your behavior, your time horizon, and whether you’re the type of person who

panic-sells at the bottom and then panic-buys at the top like it’s an Olympic sport.

The portfolio problem tactical equity tries to solve

Consider two investors with the same long-term expected return. Investor A stays the course through ugly markets.

Investor B sells when headlines scream and gets back in after markets recover.

Investor B’s return can be dramatically worseeven if they’re “right” about being scaredbecause the market’s best days and worst days tend to cluster,

and missing rebounds is costly.

In that context, a well-designed tactical sleeve can act like a behavioral bridge:

it provides a framework for “doing something” without turning your portfolio into a day-trading simulator.

It can also provide a risk-managed alternative to the “all stocks all the time” approach for investors who simply won’t stick with buy-and-hold during a severe drawdown.

Setting the right expectations (or: how to avoid being angry at math)

The fastest way to hate tactical equity is to expect it to behave like a superhero.

Tactical strategies are more like a fire extinguisher:

most of the time it sits there doing nothing interesting, and occasionally it matters a lot.

Expectation #1: Tactical can lag in strong bull markets

If your strategy reduces exposure during turbulence, it may also reduce exposure during “messy” ralliesespecially ones that whip around.

That means there will be stretches where a simple S&P 500 index fund looks like a genius and your tactical sleeve looks like it missed the memo.

That isn’t necessarily failure; it’s the fee you pay for the insurance-like feature of avoiding some large left-tail outcomes.

Expectation #2: You will face whipsaws

A whipsaw is what happens when markets fake you out: the signal says “risk off,” then markets rip higher; or the signal says “risk on,” then the market drops again.

Tactical investors must accept whipsaws the way drivers accept red lights: you can complain, but you still have to stop.

The goal is not to avoid every whipsawit’s to design a process that can survive them.

Expectation #3: Tactical is about probabilities, not perfection

Tactical equity doesn’t need to sidestep every drawdown. It doesn’t need to sell the top or buy the bottom.

In practice, many rules aim to avoid the big downtrendsespecially the prolonged oneswhile still participating in long-run equity growth.

If you expect tactical strategies to produce flawless exits and entries, you’re not investingyou’re auditioning for a role in a fantasy novel.

What part of the portfolio can tactical risk management replace?

This is where the conversation gets genuinely useful: tactical equity is not “a whole portfolio.”

It’s a component, and how you size it should reflect what job you want it to do.

Option A: Replace part of your equity allocation

Example: instead of 80% stocks / 20% bonds, you might run 60% core buy-and-hold equity,

20% tactical equity, and 20% bonds.

Here the tactical sleeve is a “shock absorber” that may reduce overall portfolio drawdowns while keeping meaningful stock exposure.

Option B: Replace part of your bond allocation (carefully)

Some investors are tempted to treat tactical equity as “equity that behaves like bonds.”

Sometimes it can lower volatility, but it’s still equity-linked risk management, not a guaranteed ballast.

If your plan depends on bonds for liquidity, stability, and rebalancing fuel, swapping them out entirely can backfire.

A more realistic approach: use tactical equity to supplement defensive assets, not eliminate them.

Option C: Use tactical as a behavior-management sleeve

If you’re the person who panics during bear markets, the portfolio’s biggest risk may not be volatilityit may be you.

In that case, a tactical sleeve can be a compromise: you keep a core buy-and-hold engine, but you also have a rules-based “plan B”

that helps you stay invested instead of rage-quitting at the bottom.

Whipsaws, drawdowns, and the emotional math of risk

Tactical equity is a trade: you exchange some upside capture for the possibility of reducing the depth and duration of drawdowns.

The problem is that investors are not robotsthey feel the trade in real time.

The whipsaw tax

Whipsaws often occur during transitionsearly bear markets, choppy recoveries, or fast shocks.

A simple “light switch” strategy (100% stocks or 100% cash) can be especially vulnerable.

That’s why many modern tactical approaches use a “dimmer switch” concept:

scale risk gradually based on the strength or breadth of signals rather than flipping the entire portfolio at once.

The drawdown problem tactical tries to improve

A deep drawdown is not just a numberit’s a behavior test. When portfolios drop 30–50%,

investors question everything: their strategy, their advisor, their life choices, and the decision to read financial news in the first place.

Tactical equity attempts to reduce the probability of those “portfolio identity crises,” even if it can’t eliminate them.

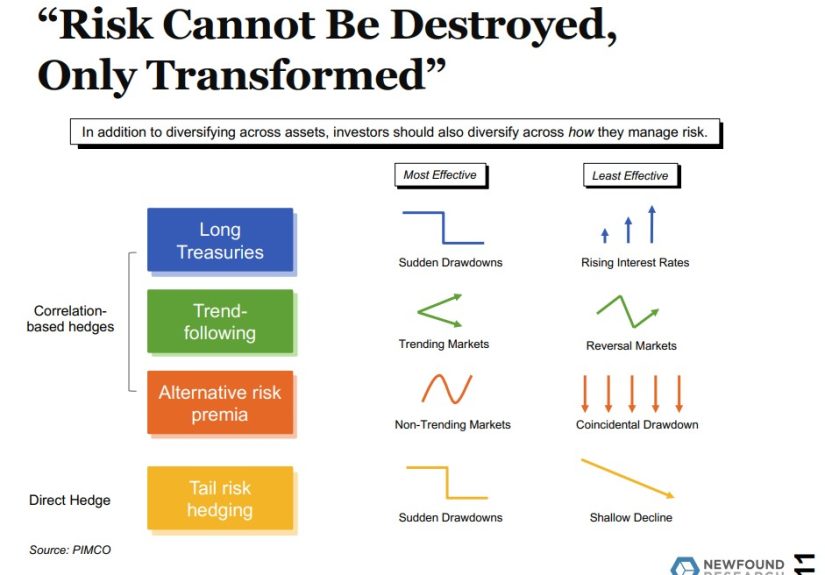

Why diversification of signals matters as much as diversification of holdings

One of the most important ideas highlighted in the Talk Your Book discussion is that diversification isn’t only about owning more stuff.

It’s also about owning more ways of being right.

Many investors diversify across asset classes (U.S. stocks, international stocks, bonds) and then run a single tactical rule across the whole thing.

That can create a hidden fragility: if your one rule has a rough decadeor if markets evolve in a way that makes that rule less effectiveyour entire “risk management”

process becomes a single point of failure.

Signal diversification in practice

- Multiple lookbacks (short-, medium-, and long-term trend/momentum signals).

- Multiple definitions of the same concept (e.g., simple vs. exponential moving averages; different thresholds).

- Multiple risk overlays (trend + momentum + volatility constraints).

- Ensemble approaches that combine many “reasonable” parameter choices rather than betting everything on one “optimal” setting.

This approach is meant to reduce what’s sometimes called specificity riskthe risk that your strategy’s success depends on a very specific rule,

calibrated to a very specific historical period, that may not repeat in the same way.

Put differently: if your entire plan hinges on the idea that “10 months is the one true moving average,” your plan might be more faith-based than you realize.

Concrete examples of tactical equity frameworks

1) The classic trend filter: moving-average timing

A widely discussed tactical concept uses a long-term moving average (often framed as a 10-month or ~200-day trend) to decide whether to hold equities or move to cash/T-bills.

The rule is simple: if the asset is above its long-term average, you stay invested; if below, you get defensive.

The appeal is obvious: it’s transparent, implementable, and designed to avoid sustained downtrends.

The drawback is also obvious: the market doesn’t care that your spreadsheet says “risk off.”

You can exit late, re-enter late, and suffer whipsaws in sideways regimes.

This is why many modern strategies seek more robust implementations than a single binary switch.

2) Momentum + trend in a global equity context

Global equity momentum frameworks rotate among equity regions (for example, U.S. vs. developed ex-U.S. vs. emerging markets) based on relative strength,

while also using trend as a risk-off filter that can shift part of the portfolio toward bonds or cash.

Conceptually, it’s trying to capture two persistent ideas: momentum tends to persist, and trends can help avoid the worst bear-market environments.

3) Risk-managed “dimmer switch” equity exposure

Another approach aims to keep equity exposure but scale itfor example, reducing risk as more signals turn negative or as volatility spikes,

rather than going instantly from “all in” to “all out.”

In plain terms: when the market starts acting like a horror movie, you don’t need to sprint out of the theater.

You can just stop buying popcorn and sit closer to the exit.

Implementation realities: fees, taxes, turnover, and the “looks easy” trap

Tactical strategies can look deceptively simple in a chart. Real life is messier.

The most common failure mode is not the mathit’s the implementation.

Trading costs and turnover

Many monthly-traded tactical models are designed to keep turnover relatively low.

But “low turnover” doesn’t mean “no costs.”

Spreads, slippage, and fund expenses still exist, and if you’re constantly tinkering, you can turn a sensible process into a commission-and-tax generator.

Taxes matter (especially in taxable accounts)

Tactical approaches can create short-term gains and higher realized distributions depending on the vehicles used.

That doesn’t mean “never do it”it means you should be intentional about where you implement it.

For many investors, tax-advantaged accounts can be a better home for strategies that trade more than a basic buy-and-hold index portfolio.

Model risk is real

Any rules-based approach can be overfit, poorly specified, or built on unrealistic assumptions.

A good tactical framework doesn’t just show a backtest; it explains:

Why should this work? What are the behavioral or structural reasons a signal might persist?

And what environments might make it fail?

A practical way to decide if tactical equity belongs in your plan

Step 1: Define the job

- Do you want smaller drawdowns?

- Do you want to reduce “time to recover” after bear markets?

- Do you want a process that helps you stay invested?

- Or are you secretly hoping to “beat the market” every year?

Step 2: Decide what you’re willing to give up

If you want protection in bad markets, you must accept some form of cost:

underperformance in certain bull markets, whipsaws, or both.

Tactical equity is a trade, not a free lunch.

Step 3: Make it boring on purpose

The best tactical strategies are often the least exciting.

They are rules-based, diversified across signals, and designed to be repeatable.

If your strategy requires you to constantly “interpret” it, it’s not a strategyit’s a vibe.

Conclusion: Tactical equity as a toolnot a personality

The Talk Your Book conversation on tactical equity is a good reminder that investing debates often miss the point.

The question isn’t “Is tactical good or bad?” The question is:

What problem are you trying to solveand what trade-offs are you willing to accept?

For investors who can truly hold through drawdowns, a low-cost buy-and-hold portfolio remains a brutally effective default.

For investors who can’teither because of behavior, time horizon, or risk capacitytactical equity can be a thoughtful sleeve,

designed to reduce the odds of catastrophic decision-making at the worst possible time.

The best version of tactical equity is not a promise. It’s a process: clear expectations, diversified signals, and a portfolio role that makes sense.

Use it like a tool. Not like a magic wand. And definitely not like a replacement for a financial plan.

Real-World Experiences (Composite Examples) With Tactical Equity

The most interesting part of tactical equity isn’t the mathit’s what happens when a real person tries to live with it.

Below are composite experiences that mirror common investor situations (not individualized advice), because tactical strategies are

basically “behavior management wearing a spreadsheet costume.”

Experience #1: The “I can’t sleep during drawdowns” investor

One common scenario is an investor who intellectually understands buy-and-hold, but emotionally experiences every bear market as a personal attack.

They don’t just see a 35% decline; they see delayed retirement, smaller college funds, and a future where they have to learn what “coupon clipping” means.

For this investor, a modest tactical sleeve (say 10–25% of the equity allocation) can provide a psychological release valve.

When markets trend lower, they see the tactical sleeve reduce risk and think, “Okay, at least something is happening.”

That feeling can be enough to keep them from dumping the entire portfolio at the bottoman outcome that matters far more than whether the tactical sleeve

beats the S&P 500 over the next 12 months.

Experience #2: The whipsaw regret spiral

Another scenario is the investor who loves tactical strategies until the first whipsaw.

Imagine a choppy year: the model reduces exposure, the market rallies, the investor feels foolish, then the model re-risking comes right before another pullback.

The investor starts “improving” the strategy: changing lookbacks, adding filters, removing filters, checking signals daily, and essentially reinventing the strategy

every time it becomes emotionally inconvenient.

The lesson here is brutally simple: tactical equity only works as intended if the investor can commit to the rules through uncomfortable periods.

If you can’t handle a strategy underperforming for a year or two, you don’t have a strategyyou have a short-term performance addiction.

Experience #3: Using tactical as a rebalancing partner

A more constructive experience shows up when tactical equity is paired with a clear portfolio framework.

For example, a household might keep a core diversified portfolio and use tactical equity as a “risk dial” rather than a replacement engine.

During extended uptrends, the tactical sleeve may maintain higher equity exposure, supporting growth.

During downtrends, it may shift partially defensive, which can create rebalancing flexibility:

the household can rebalance from the defensive sleeve into beaten-down assets systematically rather than emotionally.

In practice, the benefit isn’t that the tactical sleeve is always rightit’s that it provides a repeatable decision framework at the exact moments when human decision-making

is most unreliable.

Experience #4: The “tax surprise” lesson

Some investors discover the hidden friction of tactical strategies the hard way: in a taxable account.

Even if the strategy trades monthly and turnover seems “reasonable,” it can still realize gains, generate distributions, or create a higher tax drag than expected.

The experience usually ends with a more nuanced implementation:

keep core buy-and-hold equities in taxable accounts (for tax efficiency and long-term compounding), and house tactical sleeves in tax-advantaged accounts when possible.

This isn’t about making tactical equity “better.” It’s about making the overall plan more efficient.

Experience #5: The best use case is sometimes the simplest one

Finally, many investors come full circle: they start by wanting tactical equity as a performance weapon and end up appreciating it as a behavior tool.

The “win” becomes staying invested, keeping risk at a tolerable level, and avoiding catastrophic mistakes.

If tactical equity helps someone stick with a long-term planespecially through the kind of market stress that makes people swear off stocks foreverthat’s not a small benefit.

It’s arguably the whole game.

Important: tactical equity isn’t a substitute for an emergency fund, appropriate insurance, or a long-term financial plan.

It’s an investment approach with trade-offs. If those trade-offs match your real-world constraints and behavior, it can be useful.

If they don’t, it can become an elegant way to create frustration.