Table of Contents >> Show >> Hide

- What “the Long Run” Really Means (Hint: It’s Not 3 Years)

- Why the Long Run Feels So Hard (Even When the Math Looks Great)

- Lessons from Market History: Crises, Recoveries, and Perspective

- Rethinking Risk: Are Stocks Really “Safer” in the Long Run?

- Practical Rules for Surviving the Long Run

- Bringing It Back to “A Wealth of Common Sense”

- Real-World Experiences: What the Long Run Feels Like in Practice

- Conclusion: The Long Run Is Built One Decision at a Time

Investors love to say, “In the long run, stocks go up,” the way runners say, “It’s just one more mile.”

Technically true. Emotionally? That “one more mile” can feel like a marathon you did not sign up for.

Ben Carlson’s blog A Wealth of Common Sense has spent years unpacking what “the long run”

really means for real people with real money and real emotions. The idea behind “The Long Run Revisited”

is simple but powerful: the data overwhelmingly supports long-term investing, but the human experience of

getting from “now” to “long run” is anything but simple.

In this article, we’ll revisit the long run using a mix of market history, behavioral finance, and

practical rules of thumb. We’ll look at what the long run actually looks like in numbers, why it feels so

brutal in the moment, and how you can structure your plan so you’re still around to enjoy the payoff.

What “the Long Run” Really Means (Hint: It’s Not 3 Years)

When people first start investing, “long term” often means “until next summer.” In market terms, though,

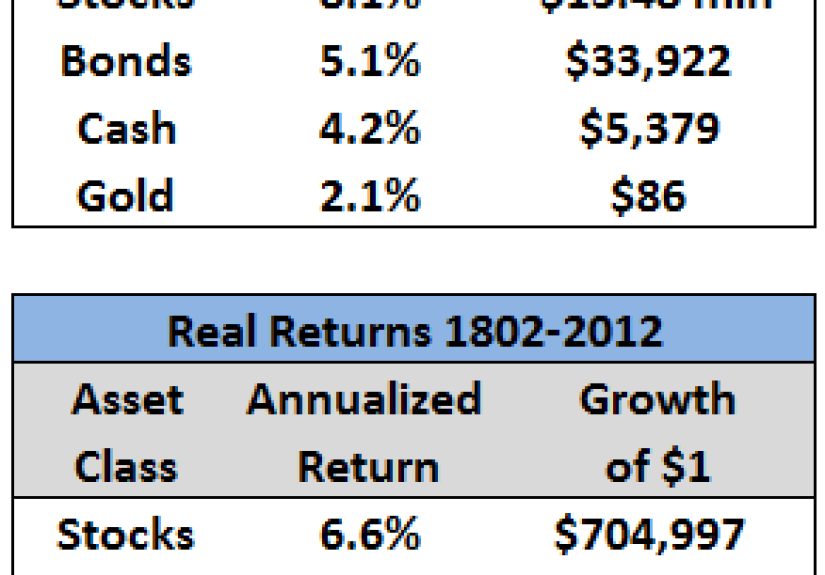

the long run is measured in decades, not seasons. Long-term stock market data for U.S. stocks shows that

the S&P 500 has delivered around 8–10% annualized returns over many decades, depending on the exact

start and end dates you choose. Over 20-, 30-, and even 40-year periods, average annual returns cluster

close to that same range, despite wildly different short-term experiences.

The takeaway: over a single year, stocks can be anywhere from “this is amazing” to “why did I do this to

myself?” Over 20 or 30 years, though, markets have historically rewarded investors who stayed the course

with far higher returns than bonds or cash, and far better odds of beating inflation.

Why Time Horizon Is Your Superpower

One of Ben Carlson’s recurring points is that younger investors don’t just have more time

they have a completely different risk profile. If you’re in your 20s or 30s, you’re not really investing

for “the market this year”; you’re investing for a world 30, 40, or even 50 years from now. That means:

- Short-term crashes are scary, but they’re largely noise on your long-term chart.

- Regular contributions matter more than the perfect entry point.

- Your human capital (your future earning power) is part of your portfolio, giving you flexibility to ride out volatility.

On the flip side, if you’re within 5–10 years of retirement, “the long run” still matters, but so does

the ride. The risk isn’t just where markets are in 30 years; it’s what happens in the early years of

retirement withdrawalsthe dreaded sequence of returns risk. A bad sequence early on can

pressure your nest egg even if long-run averages eventually look fine.

Why the Long Run Feels So Hard (Even When the Math Looks Great)

Pull up a 100-year stock market chart and it looks like a gentle upward slope. Live through it in real

time, and it feels like an emotional roller coaster designed by someone who hates you.

Volatility Is a Feature, Not a Bug

Long-run data shows a clear pattern: over 1-year periods, stock returns are all over the placehuge gains,

painful losses, and everything in between. Over 10-, 20-, or 30-year periods, the distribution narrows and

the odds of a negative return shrink dramatically. That doesn’t mean risk disappears; it means the payoff

for staying invested becomes much more reliable.

Historically, U.S. stocks have beaten safer assets like bonds and cash over most 20- and 30-year windows.

But in the middle of that window, you can get hit with recessions, bear markets, rate shocks, tech bubbles,

financial crises, pandemics, and headlines that sound like the world is ending. That discomfort is the

price of admission for long-run returns.

The Behavioral Tax: Why We Pay for Our Own Impulses

The hard part isn’t understanding that “time in the market beats timing the market.” The hard part is

sitting still when everything in your body screams “do something!”

Behavioral research shows that:

-

Many investors underperform the very funds they invest in because they buy high (when things feel safe)

and sell low (when things feel scary). -

The average investor often misses a handful of the best days in the market because those days tend to

come clustered around the worst dayswhich is precisely when people are most likely to bail. -

Fear, pain, and anxiety shrink our time horizons. When markets are down, a 30-year plan suddenly feels

like a 30-day emergency.

In other words, the enemy isn’t just volatilityit’s how we react to it. The “long run” only works if you

actually stay invested long enough to experience it.

Lessons from Market History: Crises, Recoveries, and Perspective

To revisit the long run honestly, you have to look at the bad times too. History is full of periods when

it felt like stocks would never recover: the Great Depression, the 1970s inflation era, the dot-com bust,

the 2008 financial crisis, and the COVID crash in 2020, to name a few.

What do these episodes have in common?

-

Each felt unique and terrifying in the moment. There were always convincing arguments

that “this time is different” and that the system was broken. -

Markets eventually recovered and moved on to new highs. Not instantly, not smoothly,

and not without real damage along the waybut they did recover. -

Investors who stayed diversified and continued investing were rewarded. Those who sold

at the bottom often locked in losses and missed the sharpest parts of the rebound.

Long-run investing is not about pretending crises don’t happen. It’s about acknowledging that crises are

part of the deal and building a plan that assumes we’ll see more of them.

Rethinking Risk: Are Stocks Really “Safer” in the Long Run?

One popular claim is that stocks become “less risky” over long periods. There’s some truth and some

nuance here.

Historically, the probability of a negative return has declined as your holding period increases. Hold

stocks for one year, and you can easily lose money. Hold them for 20 or 30 years, and the odds of a

negative real (inflation-adjusted) return have been much lower.

But “lower odds of losing money” does not mean “guaranteed outcome.” The long run:

- Reduces the range of likely outcomesbut you can still land in the lower part of that range.

- Doesn’t protect you from bad timing if you’re forced to sell at a specific moment (retirement, job loss, big expense).

- Still requires a sensible asset mix; 100% stocks may not be appropriate for every long-term investor.

The better way to think about it: stocks offer a risk premiumhigher expected returns in

exchange for living with volatility and uncertaintyeven over long horizons. The long run doesn’t

eliminate risk; it rewards those who can bear it intelligently.

Practical Rules for Surviving the Long Run

Revisiting the long run is useful only if it leads to better decisions. Here are practical guidelines

inspired by long-term market data and common-sense investing principles.

1. Match Your Investments to Your Time Horizon

Money you need in:

- 0–3 years: Keep it in cash, high-yield savings, or short-term bonds. This is “sleep at night” money.

- 3–10 years: Consider a balanced mix of stocks and bonds. You want growth, but also protection.

- 10+ years: This is prime stock territory. The longer the horizon, the more sense it makes to lean into equities.

One of the biggest mistakes is using “retirement” as a single date. In reality, retirement can last 20–30

years or more. That means a good portion of your money still has a very long time horizon, even as you’re

drawing from your portfolio.

2. Automate Contributions and Take Timing Off the Table

Dollar-cost averaginginvesting a fixed amount at regular intervalssounds like a boring idea until you

realize it’s basically a psychological hack. You:

- Buy more shares when prices are low and fewer when they’re high.

- Stop obsessing over whether “now” is the right time to invest.

-

Turn volatility from something you fear into something that quietly works in your favor over time

(assuming you keep buying).

Automation is your friend. The less you have to manually decide when to invest, the less likely you are

to talk yourself out of doing the right thing.

3. Diversify So You Can Stay in the Game

Diversification isn’t about maximizing bragging rights; it’s about survival. A diversified portfolio:

- Spreads your risk across sectors, regions, and asset classes.

- Reduces the chance that a single stock or theme can derail your plan.

- Makes volatility more tolerable, which increases the odds that you actually stick with your strategy.

A simple mix of broad stock index funds and bond funds can be surprisingly powerful. The goal is not to

win every year; it’s to avoid losing the decade.

4. Decide in Advance How You’ll React to Bad Markets

The worst time to design your plan is in the middle of a panic. Instead, revisit the long run now and

decide:

- How much of a drawdown you can mentally tolerate (for example, “I can live with a 20–30% drop”).

- How you’ll rebalance during bear markets (for example, “if stocks are down 25%, I’ll rebalance back to my target mix”).

- What headlines you’ll ignore on principle (“I don’t make portfolio changes based on short-term forecasts”).

Write your rules down. Future you, sitting in front of a scary red chart, will be grateful.

5. Revisit, Don’t React

“Staying the course” doesn’t mean never touching your portfolio again. Life changes: you age, your income

changes, you take on responsibilities, you may care more about stability than maximizing every last basis

point of return.

A healthier approach:

- Review your plan once or twice a year, not every time the market moves.

- Adjust your risk level gradually as your time horizon and goals evolve.

- Keep costs low so more of the long-run return shows up in your account, not in someone else’s.

Bringing It Back to “A Wealth of Common Sense”

“The Long Run Revisited” is really about recalibrating expectations. Yes, long-run data is encouraging.

Yes, stocks have historically rewarded patient investors. But no, that doesn’t mean the journey is smooth,

easy, or guaranteed.

A wealth of common sense in the long run looks like this:

- Accept volatility as the cost of higher returns, not as a sign the system is broken every time markets fall.

- Use time as your ally by matching your investments to your real-life horizons.

- Automate good behavior and remove as many emotional decisions as possible.

- Plan for bad markets in advance so you’re not improvising in a crisis.

- Remember that your goal is not to beat the market every yearit’s to meet your own financial goals over a lifetime.

The long run isn’t something that magically arrives; it’s something you build, one contribution and one

rational decision at a time.

Real-World Experiences: What the Long Run Feels Like in Practice

Theory is nice. Charts are pretty. But what does the long run actually feel like for real investors?

The New Investor Who Started at the “Worst” Time

Imagine someone who started investing a few years before a major downturnsay, before a big recession or

a crisis. At first, things go great: green arrows, growing balances, the intoxicating feeling that you’re

finally “good with money.”

Then the downturn hits. Suddenly, contributions feel like throwing good money after bad. Each paycheck

contribution buys more shares at lower prices, but it feels like you’re just feeding a machine that only

spits out disappointment.

Fast-forward a decade. That same investor looks back and realizes those painful contributions during the

downturn were actually the most profitable dollars they ever invested. They bought when valuations were

cheap and sentiment was terrible. In the moment it felt like a mistake; in the long run it turned into

opportunity.

The Near-Retiree Facing Sequence Risk

Now imagine someone five years from retirement. They’ve done the hard partsaved consistently for decades.

But even after a lifetime of investing, the final stretch can be nerve-racking.

If they keep 100% of their portfolio in stocks and a major bear market hits right before or right after

they retire, withdrawals can compound the damage. That’s sequence of returns risk in real life: the order

of returns suddenly matters as much as the average.

A more resilient approach might be:

- Gradually shifting a portion of the portfolio into bonds and cash as retirement approaches.

- Maintaining a “cash bucket” to cover a few years of spending, so they don’t have to sell stocks at fire-sale prices.

- Being flexible with withdrawals during rough patchesmaybe tightening the belt slightly when markets are down, then loosening it when they recover.

The long run doesn’t end at retirement. It simply moves into a new phase where protecting the sequence of

returns becomes part of common sense.

The Emotionally Intelligent Investor

One of the most underrated long-run skills isn’t mathit’s self-awareness.

The emotionally intelligent investor:

- Knows their own pain points. Maybe a 50% drop would make them abandon ship, but they can live with 20–30%.

- Chooses an asset mix they can actually stick with, even if it means slightly lower expected returns on paper.

- Curates their information diet, limiting doom-scrolling and hot takes that inflame anxiety.

They’re not trying to be a robot. They’re trying to design a system that accounts for the fact that they’re human.

Why “Revisited” Matters

The phrase “The Long Run Revisited” implies we’re coming back to something we thought we understood. That’s

exactly what smart investors do. They revisit their assumptions:

- Is my definition of “long term” still realistic for my age and goals?

- Can I still handle the risk I’m taking, or have my circumstances changed?

- Have I drifted into speculation instead of investing without realizing it?

Revisiting the long run isn’t a sign of doubtit’s a sign of maturity. Markets change, life changes, and

your plan should evolve with both.

Conclusion: The Long Run Is Built One Decision at a Time

The long run is where market history looks clean and reassuring. Real life is everything that happens on

the way there: the crashes, the recoveries, the boring middle years when nothing dramatic happens, and

the countless small decisions you make about saving, spending, and staying the course.

A wealth of common sense in investing doesn’t require secret formulas or perfectly timed trades. It

requires:

- Respecting the data without ignoring your own psychology.

- Using time as an ally instead of demanding instant results.

- Designing a portfolio you can live with in bad times, not just admire in good times.

- Revisiting your plan periodically so it matches the life you’re actually living.

The long run is not a place you magically arrive at someday; it’s the cumulative result of countless

ordinary, rational decisions. Revisit it often, commit to it fully, and let common sensenot fearset the

pace.