Table of Contents >> Show >> Hide

- John Bogle’s Greatness: He Made “Keeping More” a Strategy

- Vanguard’s Not Just an Index Fund ShopIt’s a Low-Cost Shop

- The Vanguard Structure: Weird (In a Good Way)

- Costs: The Tiny Leak That Sinks Huge Ships

- The Evidence: Why Most Active Funds Struggle to Win (After Fees)

- The Behavioral Edge: “Stay the Course” Is a Superpower

- How to Build a Bogle-Style Portfolio (Without Becoming a Finance Monk)

- The “Vanguard Effect”: When One Firm Forces Everyone to Compete on Price

- Common Misconceptions Bogle Would (Politely) Roast

- Real-World Experiences Related to Bogle & Vanguard (500+ Words)

- Experience #1: The relief of a portfolio that doesn’t require constant babysitting

- Experience #2: The “fee awakening” moment

- Experience #3: The “I thought I could time it” loop

- Experience #4: The surprise of how “average” becomes impressive over time

- Experience #5: The calm confidence that comes from a repeatable process

- Wrap-Up: The Greatness Is in the Boring Stuff

If personal finance had a “boring superhero” category, John C. Bogle would be wearing the capeexcept he’d refuse

the cape because it would add unnecessary cost. And then he’d negotiate the cape’s expense ratio down to 0.00%.

Ben Carlson once framed it perfectly: you could do better than Vanguard, but you could also do much worse.

That’s the magic. It’s not that Vanguard offers a secret investing cheat code. It’s that Bogle’s whole philosophy

makes it harder for you to sabotage yourself while the market does its long-term thing.

John Bogle’s Greatness: He Made “Keeping More” a Strategy

Before Bogle became a legend in investing circles, he was a guy with an unglamorous obsession: costs. Not

“coupon-clipping for fun” costsinvestment costs. The kind that don’t scream at you from your monthly statement

but still quietly siphon off your future.

Vanguard began operations in 1975, and the firm’s origin story isn’t “we wanted to maximize shareholder value”

so much as “we wanted investors to stop getting fleeced by layers of fees.” A year later, Vanguard helped

popularize indexing for everyday investors with what became the Vanguard 500 Index Fundan idea so unsexy that it

was mocked as settling for mediocrity. Today, the joke’s on the mockers (and the punchline is compounding).

Vanguard’s Not Just an Index Fund ShopIt’s a Low-Cost Shop

Here’s a subtle point that matters more than it sounds: Vanguard isn’t “only” index funds. It offers both active

and passive strategies. The brand’s superpower is that it has been designed around low costsand

that’s a different promise.

Carlson highlighted this distinction years ago: people assume Vanguard equals indexing. In reality, the core

identity is “low-cost investing,” with indexing as the most famous expression of that identity. Think of it like

this: indexing is the pizza. Low cost is the oven that keeps making it cheap, reliable, and hard to ruin.

Why “low-cost” beats “hot-stock-picker” in the long run

Investing is one of the few places where paying more often buys you… a fancier explanation for why you didn’t do

better. Bogle’s point wasn’t that every active manager is incompetent. It’s that the math is stacked:

before costs, investors as a group earn the market’s return; after costs, the

group earns less. And somebody collects the difference.

The Vanguard Structure: Weird (In a Good Way)

Vanguard’s structure is famously different. The company is owned by its funds, and the funds are owned by the

shareholders who invest in them. In plain English: Vanguard doesn’t have outside public shareholders demanding

bigger profit margins the way many financial firms do.

That doesn’t mean Vanguard is a charity. It does mean the incentives are different. When the firm benefits from

economies of scale, the logic of the structure pushes that benefit toward investors through lower fees and

lower-friction productsrather than pushing it toward external owners.

Costs: The Tiny Leak That Sinks Huge Ships

Fees are the most underrated villain in personal finance. Not because they’re mysteriousbut because they’re

quietly persistent. A one-time fee hurts. A fee that follows you around for decades like an overly attached

housecat hurts a lot more.

What “expense ratio” really means

An expense ratio is an annual cost charged by a fund, expressed as a percentage of assets. It can include

management fees, distribution fees (like 12b-1 fees), and other operating expenses. The key detail: these costs

are typically deducted from fund assets, so you “pay” them indirectly through lower returns over time.

A quick real-number example (no scary math, promise)

Imagine two investors each contribute $500 per month for 30 years. The market delivers a 7% annual return before

fund costs (not guaranteed, but a reasonable long-term illustration). One investor pays 0.05% per year; the other

pays 0.60% per year.

The difference doesn’t sound dramatic in year one. But over 30 years, that small fee gap can translate into

roughly $50,000+ less wealth for the higher-fee investor. Same market. Same contributions. Same

discipline. Different leak in the bucket.

This is why Bogle’s greatest “innovation” wasn’t predicting markets. It was changing the default conversation

from “what’s the best fund?” to “what’s the lowest-cost way to capture what markets give?”

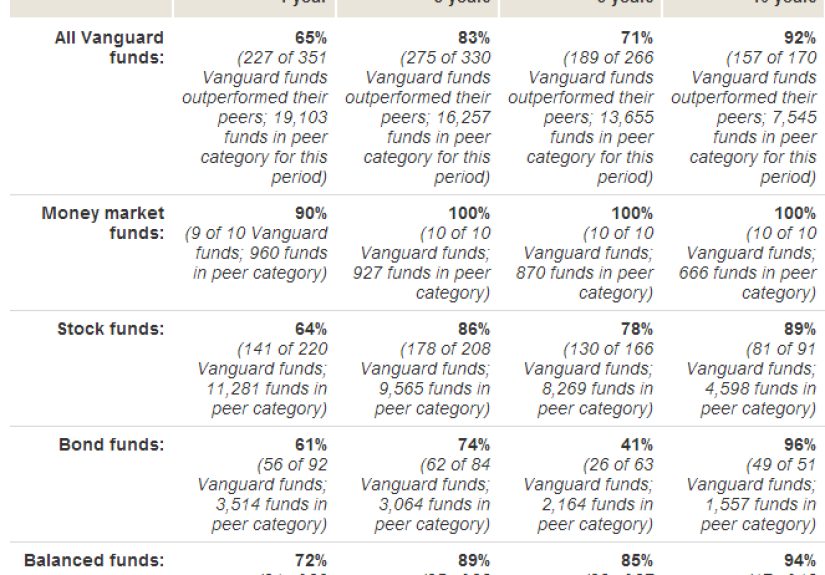

The Evidence: Why Most Active Funds Struggle to Win (After Fees)

Active management can outperform in a given year. Sometimes it does! The issue is consistencyand the brutal

reality that fees create a hurdle that never gets tired.

Large-scale scorecards that compare actively managed funds to benchmark indices repeatedly show that a majority

of active funds underperform over longer periods. It’s not because markets are perfectly efficient every second.

It’s because after costs, the bar becomes very highand the competition is fierce.

“But I only need one great manager!”

True. You only need one. You also only need one winning lottery ticket. The hard part is identifying the winner

in advance, sticking with them through rough stretches, and not switching strategies at the worst moment

(which is the default human setting).

Bogle’s approach doesn’t require predicting who will win. It assumes you’ll take the market return, minimize

avoidable costs, and let time do the heavy lifting. It’s not flashybut it’s durable.

The Behavioral Edge: “Stay the Course” Is a Superpower

Let’s be honest: the biggest threat to your portfolio may not be inflation, interest rates, or recessions. It may

be youspecifically, the version of you who checks your account after a scary headline and decides to

“do something.”

Bogle’s philosophy works partly because it reduces the number of decisions you have to get right. A simple,

diversified, low-cost portfolio doesn’t eliminate volatility. It does make it easier to hold your position when

volatility shows up (uninvited, as it always does).

Simple beats sophisticated when emotions get involved

- Complex portfolios give you more knobs to twistand more chances to panic-tweak.

- Low-cost diversified portfolios are easier to understand, automate, and stick with.

- Consistency often beats brilliance, because brilliance is hard to repeat on schedule.

How to Build a Bogle-Style Portfolio (Without Becoming a Finance Monk)

You don’t need a finance degree or a secret Wall Street handshake to apply the Bogle approach. You need a few

sensible building blocks and the willingness to be “boring” longer than everyone else.

Step 1: Decide what you’re investing for

Retirement? A house down payment? College? “I would like future-me to sleep at night”? Your timeline matters.

Money needed soon shouldn’t be riding the stock-market roller coaster with no seatbelt.

Step 2: Choose broad diversification

A classic Bogle-style setup is built from broad, low-cost index funds that cover:

- U.S. stocks (total market or S&P 500 exposure)

- International stocks (developed + emerging markets)

- High-quality bonds (to reduce volatility and provide ballast)

Many investors simplify even further by using a single target-date fund or balanced fund that automatically

handles diversification and rebalancing. The “right” answer is the one you can stick with for decades.

Step 3: Keep costs low and avoid unnecessary fee layers

Low-cost index mutual funds and ETFs have become dramatically cheaper over time. Industry research shows average

expense ratios for long-term funds have fallen for decades, with index options typically among the lowest-cost

choices.

Translation: you’re living in the golden age of cheaper investing. Please don’t ruin it by paying 1.25% for the

privilege of someone reading earnings calls dramatically into a microphone.

Step 4: Automate contributions and rebalance occasionally

Set up automatic contributions in your 401(k), IRA, or brokerage account. Make saving feel like a utility bill:

consistent, boring, and non-negotiable. Rebalance once or twice a year (or when allocations drift materially).

That’s it. No daily chart-watching required.

The “Vanguard Effect”: When One Firm Forces Everyone to Compete on Price

One of Bogle’s biggest wins is how his ideas reshaped the industry. As low-cost indexing grew, competitors had to

cut fees, launch cheaper share classes, and justify costs more clearly. Even investors who never touched a Vanguard

fund benefited from the pressure it created.

Vanguard itself reports an exceptionally low asset-weighted average expense figure for its U.S. funds and has

continued to reduce costs over time as scale and competition increased. In other words: the compounding you do

not pay for is still compounding in your favor.

Common Misconceptions Bogle Would (Politely) Roast

“Indexing is settling for average.”

Indexing is accepting the market returnwhich historically has been pretty generous over long periodswhile

reducing the odds that you underperform due to fees, taxes, turnover, and bad timing. “Average” is a weird insult

when it beats most competition after costs.

“Fees are tiny, they don’t matter.”

A fee is tiny in a single year. In a multi-decade compounding engine, a fee is a permanent drag. It’s like adding

a small hill to every mile of a marathon. You’ll still finish… just later, sweatier, and wondering who approved

this route.

“I’ll switch to low cost later.”

Later is when you’ll wish you started earlier. The point isn’t perfection; it’s direction. Reducing recurring

costs now gives every future dollar more room to grow.

Real-World Experiences Related to Bogle & Vanguard (500+ Words)

“Experiences” is a funny word in investing, because the market has a talent for giving everyone the same lesson

in a different costume. Below are real-world, commonly reported investor experiences that echo Bogle’s worldview

not personal anecdotes from one person, but patterns that show up again and again when people try to build wealth

the non-glamorous way.

Experience #1: The relief of a portfolio that doesn’t require constant babysitting

Many investors start out thinking successful investing means constant action: checking prices, following earnings,

moving money around, hunting for the next breakout stock. Then life gets busy. A career happens. Kids happen.

Sleep becomes a luxury product. At that point, the appeal of a diversified, low-cost portfolio becomes obvious:

it keeps working even when you’re not watching it.

This is the underrated value of a Bogle-style approach: it’s compatible with being a human who has weekends,

hobbies, and a nervous system. A simple mix of broad index funds (or a single all-in-one fund) reduces decision

fatigue. It also reduces the temptation to tinker during scary markets, which is exactly when tinkering tends to

be most expensive.

Experience #2: The “fee awakening” moment

A lot of people don’t realize what they’re paying until they see it in plain language: an expense ratio, a sales

load, a 12b-1 fee, an advisory fee stacked on top of fund fees, or account costs that feel like “small potatoes”

each month. The awakening often happens when someone compares two similar fundsboth diversified, both mainstream

but one costs 0.05% and the other costs 0.90%. The higher-cost option has to be dramatically better just to tie.

And tying is not the dream.

After this moment, investors often become lifelong fee-minimizersnot because they’re cheap, but because they

finally understand fees are the one part of investing you can control with near certainty. You can’t control what

the market does next year. You can control whether you pay an extra half-percent every year for decades.

Experience #3: The “I thought I could time it” loop

Another common experience is the timing loop: someone exits the market after a drop to “wait for clarity,” then

waits too long because clarity is always late, then buys back after prices recover because the news feels safer

effectively selling low and buying high with extra steps.

Bogle’s approach is basically an anti-loop device. When your plan is “own the market, keep costs low, contribute

consistently,” you spend less time trying to predict headlines and more time doing the boring actions that

compound: saving, investing, rebalancing, and letting time work.

Experience #4: The surprise of how “average” becomes impressive over time

Early on, indexing can feel underwhelming because it doesn’t deliver bragging rights. You can’t say, “I spotted

this hidden gem at $12.” What you can sayeventuallyis, “I participated in decades of global economic growth

while paying very little for the privilege.” That’s not a great party line, but it’s a fantastic retirement plan.

Over long stretches, the combination of diversification, low costs, and consistent contributions often produces a

result that looks almost magical to people who spent years chasing hot strategies. It’s not magic. It’s math plus

behavior.

Experience #5: The calm confidence that comes from a repeatable process

The final experience is psychological: a sense of calm. Investors who adopt a low-cost, rules-based process often

report they feel less anxious during market storms because they’re not relying on being “right” about what happens

next. Their confidence comes from having a plan that doesn’t require prediction. They know downturns happen. They

know recoveries happen. They know costs matter every year, in good markets and bad. And they know their system is

built to survive those cycles.

Wrap-Up: The Greatness Is in the Boring Stuff

John Bogle’s legacy isn’t a clever trade, a viral prediction, or a once-in-a-generation market call. It’s the

simple, stubborn insistence that investors deserve a fair shakeand that “fair” often looks like low costs, broad

diversification, and the discipline to stay the course.

If you need a weekly reminder, make it this: you don’t have to win every day. You just have to avoid losing

unnecessarily. Keep what you can control (costs, diversification, behavior) working in your favor, and let the

market handle the rest.